Chavalit Nimlaor

Administration and Management College, King Mongkut`s Institute of Technology, Ladkrabang, Thailand

Jirasek Trimetsoontorn

Administration and Management College, King Mongkut`s Institute of Technology, Ladkrabang, Thailand

Wanno Fongsuwan

Administration and Management College, King Mongkut`s Institute of Technology, Ladkrabang, Thailand

Research Journal of Business Management

Year: 2015 | Volume: 9 | Issue: 1 | Page No.: 25-46

ABSTRACT

This study is concerned with the analysis of factors that affect the AEC garment industry and Thailand’s ability to compete within it. Given the 2035 projected 850 million AEC consumer market along with the tripling of economic output by 2025, the ramifications of policy are enormous for both Thailand and the garment industry’s competitiveness. Therefore, this study was undertaken to conduct analysis and structural equation modeling of the variables from membership input from the Thai Garment Manufacturers Association (TGMA). The importance of this study can’t be underestimated, as Thai garment exports in 2012 declined to US$2.8 billion while textile exports dropped to US$3.5 billion, 10 and 15% drops, respectively. Study results however found that to maintain competitiveness, larger industry members are expanding their operations by relocating their production to lower wage members of the AEC such as the CLMV countries of Cambodia, Laos, Myanmar and Vietnam while smaller Thai garment industry SMEs have already ceased trading. Although, the trend is negative for Thailand’s garment enterprises, factors studied which can influence change and growth include leadership, investment, teamwork and R and D. Given greater understanding of these variables, Thailand can challenge global players and create brands that overcome what otherwise appears to be a continued contraction and loss of competitive advantage. Using decades of industry knowledge, researchers obtained quantitative data from 178 entrepreneurial TGMA members while qualitative data was gathered from in-depth interviews of 10 senior industry executives.

PDF Abstract XML References Citation

How to cite this article

Chavalit Nimlaor, Jirasek Trimetsoontorn and Wanno Fongsuwan, 2015. AEC Garment Industry Competitiveness: A Structural Equation Model of Thailand’s Role. Research Journal of Business Management, 9: 25-46.

DOI: 10.3923/rjbm.2015.25.46

URL: https://scialert.net/abstract/?doi=rjbm.2015.25.46

DOI: 10.3923/rjbm.2015.25.46

URL: https://scialert.net/abstract/?doi=rjbm.2015.25.46

INTRODUCTION

The garment industry is one of the oldest and largest export industries and it exemplifies the growth in global manufacturing. Many economies produce textiles for the international market, making this among the most global of all industries (Dickerson, 1995) with about 50% of apparel sold in the U.S being made abroad (Deloitte, 2004).

Globalization today means that economic activity is not only international in scope but also global in organization. With production dispersed geographically to a great many locations across and within countries, the garment sector is emblematic of the global manufacturing system (Gereffi, 1994). The relative ease of setting up apparel firms, coupled with the prevalence of developed country protectionism in this sector, has led to the unparalleled worldwide dispersal of production and exporting in this sector.

Supplier dependence on larger retailers, particularly companies such as Wal-Mart, Costco and Target, is reshaping almost every aspect of the apparel industry and footwear business model which is ultimately changing how companies create, produce and deliver goods (Deloitte, 2004).

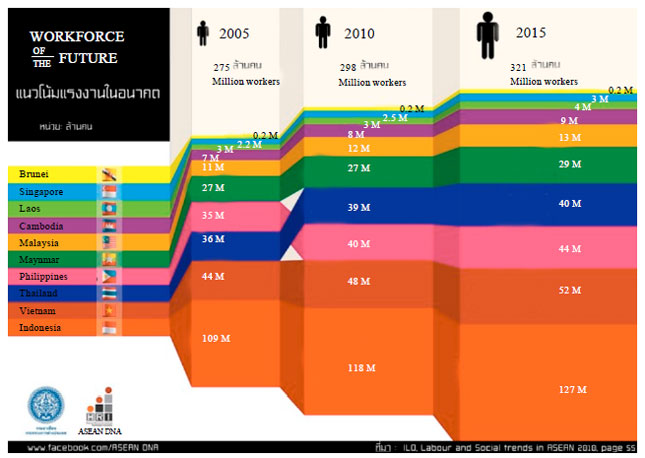

With this off-shoring and outsourcing process, much of which is to Asia and the AEC, work force potential is significantly higher than that of either the European Union or the USA (Fig. 1 and 2).

| |

| Fig. 1: | ASEAN Work Force (in millions) current vs. in-coming work force in the next 15 years. Source: ASEAN Secretariat CIA World Fact book (2012) |

| |

| Fig. 2: | ASEAN workforce of the future. Source: PMAP (2010) |

As can be seen from the accompanying two figures to the left, ASEAN’s 10 nation workforce presently has over 400 million workers with another 171 million projected over the next 15 years. That is in comparison to the EU with only 338 million and the USA with 209 million (Fig. 1). Additionally the median age of the population in Southeast Asia is 28 years old, compared to Germany’s 45. No matter how you look at it, as a regional block, the AEC is a looming powerhouse of both economic and worker might. In the middle of all this is Thailand which has functioned as the hub for much of this growth and expansion which in 2015 is projected to have 40 million workers (Fig. 2).

The ASEAN Economic Community’s (AEC) implementation of a “Single-window” common market system by 2015 has pushed the countries in the region to innovate and forge more partnerships with like-minded investors to create a vertical production network for the textiles industry. An integrated regional production network allows each country to focus on specific components, creating one ASEAN supply chain. Vertical integration means less competition among countries as the markets work towards harmonized production.

The ASEAN Federation of Textile Industries (AFTEX), a group of textile and garment associations of the 10 ASEAN member countries, launched the Source ASEAN Full Service Alliance (SAFSA) in 2010 (USAID, 2010). The SAFSA works on linking ASEAN apparel factories to create a virtual vertical supply chain between buyers, textile mills and apparel factories, enabling businesses to offer a complete service package to international buyers.

Developed and managed by the United States Agency for International Development’s (USAID’s) VALUE Project in partnership with the ASEAN Federation of Textile Industries (AFTEX), SAFSA officially launched in April 2010 with the induction of 14 virtual vertical factories (VVFs) as founding members. SAFSA is not a company per se. As its name suggests, SAFSA is an alliance of companies committed to positioning Southeast Asia as a competitive, full-service source of quality garments.

Source ASEAN Full Service Alliance has 45 members trading among themselves including 27 buyers with over US$ 50 billion in annual apparel sales. Some of the major brands that are SAFSA customers are the Benetton Group, Colombia Sportswear Company, Debenhams, Guess, Marks and Spencer, Polo Ralph Lauren and Hermes-OTTO (ASEAN, 2013).

Textile is one of the largest export products from ASEAN, amounting to almost US $10 billion in 2011 (ASEAN, 2013), with exports from Thailand in first 9 months of 2012, represented $2.15 billion USD according to the Thai Garment Manufacturers Association (TGMA) (Tuan, 2013). Additionally, the 10 nation AEC’s economy will triple by 2035 along with a population expansion of almost one-quarter by 2035 to 850 million people.

Thailand, with a population of 66.7 million today, contributed over 1 million workers to the 2008 economy through the garment and apparel sector (Fig. 3). Today that number is dropping rapidly.

However, several other ASEAN member states are benefiting from the industry’s export growth and Thailand’s loss of competitiveness. In the first quarter of 2013 alone, Viet Nam’s garments and textiles exports reached US$3.7 billion or a year-on-year rise of 18.3%. The country’s largest importer has been the ASEAN market itself which contributed US$ 111.4 million to Viet Nam’s exports, a 44.4% year-on-year increase. This increase in inter-region trade of goods foreshadows the importance of ASEAN not just as an exporter but also as a market.

The Lao PDR has also improved their game attracting orders from investors who used to import from China. Comparing the years 2011 and 2012, Lao’s export to Canada and Japan increased by 34 and 60%, respectively (ASEAN, 2013).

| |

| Fig. 3: | No. of workers (2008). Thailand Textile Industry Statistics (TTI, 2007) |

Meanwhile, Cambodia has established itself as a credible producer. The United Nations’ International Labor Organization independently monitors and reports on working conditions in the Cambodian textile factories according to local and international standards which encourages companies like Levi’s, Gap, Sears, Wal-Mart and Disney to choose Cambodia as their manufacturing hub.

The garment and textile industry in the Kingdom of Cambodia-a Southeast Asian country bordered by Thailand, Laos, Vietnam and the Gulf of Thailand-was established in 1993 when foreign investors set up manufacturing there. It is the largest foreign exchange earner in Cambodia and a significant contributor to its economy. Garment production accounts for 16% of Cambodia’s total Gross Domestic Product (GDP) and employs 45% of its manufacturing workers (Thomasson, 2013).

Today, Cambodia has over 300 garment factories with AFTEX data showing Cambodia opening one textile factory per week. Cambodia’s textile industry employs around 280,000 workers and accounts for 85% of Cambodia’s total exports. The US and Europe absorbs the largest chunks of its exports at 66 and 22%, respectively (ASEAN, 2013).

While Cambodian garment exports rose 10.2% to US $5.48 billion in 2012, the increase of raw materials imported to support this growth increased about 20% from US $2.6 billion in 2011 to US $3.1 billion in 2012, according to figures from the Ministry of Commerce (Phnom Penh Post, 2013). Additionally, electricity costs are the simple answer to a lack of raw material production and that this is not a new phenomenon with investors anxiously waiting reduced power costs.

Thai garment exports for 2012 fell by 10% to US$2.8 billion while the country’s textile exports dropped by 15% to US$3.5 billion (Dyson, 2012). Thailand has around 4,500 textile and apparel factories employing almost a million workers (Fig. 4) and according to the Thailand Textile Institute’s (THTI’s) 2010-2011 Thai Textile Statistics report, the textile subsector accounted for approximately 3.4% of the country’s total gross domestic product in 2009 (Thomasson, 2012).

These factories range from man-made fiber plants, spinning and weaving, to dyeing and printing. Some of these are involved in ASEAN’s integrated supply chain such as Bangkok Weaving Mills Groups which delivers pre-dyed fabrics by road to Cambodia, where another factory cuts and sews them for Benetton (ASEAN, 2013).

Thailand’s clothing industry uses a comprehensive and complete production and supply chain cycle which is totally integrated. It delivers products into the upstream, midstream and downstream markets. The industry is fully integrated, meaning it has an upstream sector (synthetic fiber and yarn manufacturing), a midstream sector (manufacturing fabric, spinning, weaving, knitting, bleaching and dyeing) and a downstream sector (apparel manufacturing).

| |

| Fig. 4: | Thai garment companies relocating to other ASEAN countries (2012) |

Apparel has been the largest sector in terms of production, employment and, for a long time, export value. But since 2007 the export value of textiles has exceeded that of apparel (SourceAsean, 2010).

It appears however that Thailand’s garment export industry is in a perpetual state of decline, losing its ranking in the competitive and intense global market. In the first nine months of 2013, Thailand experienced a negative growth which was seen in most major product groups, including cotton garments (down 8.8% to $463.8 m USD), man-made fibre garments (down 3.1% to $629.3 m USD) and fabrics (down 2.5% to $408.3 m USD) with the US, EU and Japan being Thailand’s largest export markets. During the 2013 January-September period, exports to the US edged up 1% to $778.9 m USD and to Japan rose 5.4% to $294.6 m USD. But these gains were offset by a 14.1% slump in shipments to the EU which fell to $512.7 m USD (Tuan, 2013).

Research in 2012 for this study discovered that employment in the Thai garment sector found that 46% of the companies had only local (Thai) employees while 54% employed both Thai and foreigners. Of these same companies, 7% employed fewer than 10 persons, 22% employed 10-100 while 25% employed over 100 persons of which 45% were foreign (Fig. 5).

For large Thai garment exporters, labor costs and worker shortages are serious hurdles to overcome within domestic markets. Therefore, Thai government officials need to also support these larger operations so they can move their production to lower costs Asean labor markets such as Vietnam, Cambodia, Myanmar, Laos and Indonesia. This can occur individually or together which will lower their start-up, logistic, infrastructure and human resource development costs (DIPP, 2012). Even though the larger 15 companies have already relocated much of their manufacturing operations into foreign ASEAN markets, they still must maintain their high value operations in Thailand which includes administrative and marketing operations as well as R and D and quality control.

| |

| Fig. 5: | Thailand garment industry 2012 foreigners and Thais working in the Thai garment sector |

It is very difficult for small and medium sized (SMEs) garment factories which have less than 200 workers to compete with larger garment manufacturers in Thailand, especially since these larger operations have access to lower cost facilities in foreign countries. The government needs to support and work closely as a team with these SMEs factories to extend investment cooperation which would help share the cost of management and promotion as well as research and development (R and D).

Proof that Thai governmental support for a manufacturing sector reaps great rewards can be found in recent statistics from ‘Cluster’ leather branding. Here we find 27 shoe manufacturers organizing with support from the Industrial Promotion Department, creating a local brand name to increase value for retail and wholesale trade in local and regional markets. This strategy improves the capability of the industry ahead of the integration of the Asean Economic Community by the end of 2015 (Thailand Environment Institute, 2003).

Additionally, foreign competition has several cost advantages including raw materials and cheaper labor costs (Padol, 2010). This problem is further exacerbated by the fact that many Thai fabric manufacturers export low quality, undyed material which is referred to as ‘grey fabric’. Partially as a result of this, Thailand’s garment exports fell 4.1% in the first nine months of 2013, according to figures from the Thai Garment Manufacturers Association (TGMA). Compared with same period in 2012, exports slipped to $2.15 bn from $2.25 bn, the association said (Tuan, 2013).

Additionally, Thailand’s garment factories which produce for export have to import significant amounts of material referred to as ‘feedstock’. Further problems are in rising labor costs and shortage of skilled labor which are considered difficult problems to overcome within the industry. The country cannot produce high-value apparel without inducing increased labor costs. Moreover, ASEAN competitors continue to undercut Thai labor, thereby forcing even a further erosion of Thai export orders.

According to the Bank of Thailand (2012), in the textiles and garments sector: Higher production costs and weakening competitiveness forced many manufacturers to move their production base to neighboring countries (Fig. 4). They also faced lower external demand following the global economic slowdown. The traditional low cost labor advantage has now moved to other countries such as Vietnam and the Bangladesh causing a decline in economic value to an economy mainly in terms of employment (Kelegama and Wijesiri, 2004).

Other Thai garment industry issues include rapid, severe and unexpected international change requiring enterprises to have a sustainable strategy to gain a competitive advantage.

The Thai apparel industry is one industry that will require an appropriate strategy for the rapidly changing environments, such as a company relocating to Hong Kong and investing in China which as a trend is nothing new, as San Martino, a European manufacturer of high-quality fashion wear, shifted its subcontracting from Belgian companies to manufacturers in Thailand which is an example of relocation of industrial activities from Europe to Asia (Cuyvers and Lenart, 1999).

Traditional order qualifying factors of price, quality and on time delivery are only the entry qualifications into the global market as today, innovativeness, design, quick response and flexibility are the requirements for a winning strategy (Weerarathne, 2004; Christopher et al., 2004).

Global fashion brands are moving to China and other developing ASEAN nations (CLMV) due to their own dramatically rising domestic production costs. According to a report from the Thai OIE (2012) in the Ministry of Industry, it found that internal and external factors affect textile and apparel markets in Thailand as well. They consist of:

| • | Baht appreciation making textiles and clothing more expensive in Thailand |

| • | Raw material prices increasing, including cotton and synthetic fibers. Increasing transportation also adds to higher production costs |

| • | Labor shortages within the industry, contributing to manufacturers being unable to supply the demand |

| • | Trade liberalization which increases cost and contributes to higher textile prices in both domestic and foreign markets, especially China |

| • | The increase of the daily minimum wage to 300 baht day-1 which started on April 1, 2012. This also included a monthly starting salary guarantee of a minimum of 15,000 baht for an individual holding a university/college degree. This began shortly after the minimum wage increase in March 2012. This inevitability adds a significant cost to the labor intensive textile and apparel market, increasing the production cost as well. The business environment in both domestic and foreign markets has changed due to the above mentioned factors leading to a heightened interest on further research on the subject |

Factors that influence the organization and strategy of the garment industry in Thailand affect the domestic apparel industry as a whole. The ongoing objective of this study is to study the relationships and influencing factors of leadership, investment, teamwork and R and D and how they influence the competitiveness of the Thai garment industry, both within in the AEC and globally. The researchers believe that this study and analysis will benefit both companies and the Thai apparel/garment market and could play a useful role to government officials in providing support, financial subsidies and guidance in how to increase the future competitiveness of the Thai apparel/garment industries.

CONCEPTUAL DEVELOPMENT

Teamwork: From the literature it can be determined that there is wide consensus about the defining factors of teams. Katzenbach and Smith (1993) stated that “A team is a small number of people with complementary skills who are committed to a common purpose, performance goals and approach for which they hold themselves mutually accountable”. In addition, regular communication, coordination, distinctive roles, interdependent tasks and shared norms are important features (Ducanis and Golin, 1979; Brannick et al., 1997).

Most commonly, teams are viewed as a three-stage system where they utilize resources (input), maintain internal processes (throughput) and produce specific products (output). Assuming this model, the necessary antecedent conditions (input) together with the processes (throughput) of maintaining teams define the characteristics of effective teams. Analysis of antecedent conditions and team processes often highlight issues for team development and training. In contrast, outcomes (output) are generally used to judge or evaluate team effectiveness.

Teamwork is defined as having three characteristics in making an effective team. They are organizational, individual and team function (Hackman, 1990; West, 1994; Brannick et al., 1997). This tripartite analysis (Table 1) can be linked with the systems model of teamwork, where organizational structure and individual contributions refer to antecedent conditions (input) and team processes generally refer to throughput.

Teamwork also contributes to the success of the organization and managers are required to use benefits wisely as a way to promote and protect employee well-being. It is thought that supporting the staff will affect their commitment to the company, thereby giving their best performance (Piriyakul, 2010). These techniques contribute to better teamwork, raising productivity and increasing the yield per unit (Keane and Te Velde, 2008). In addition, the size of the business affects the operations of the business. It has a positive and direct effect on policy and the quality of service and operational results (Ladda, 2012).

Teamwork and collaboration are also key elements which also includes membership within both the team and the company. This draws out the greatest potential of the employee which benefits the organization and good managers will recognize the uniqueness and differences their team members.

Leadership: Based on the analysis of many researchers, business leaders must possess strategic vision abilities and set goals the organization can reach. They must also have a strategy for use in both day-to-day and strategic operations. This ability will have an impact on the direction of the market, corporate performance and gross sales. It will also affect the success of product and services, cost recovery and the ability to retain customers and the controlling of operational costs (Subramanian and Gopalakrishna, 2001; Asiegbu et al., 2012) by determining direction.

Leadership is needed when the task becomes more dynamic and complex. Leaders need to maintain a strategic focus to support the organization’s vision, facilitate goal setting, educate and evaluate achievements (Barczak, 1996; Proctor-Childs et al., 1998).

| Table 1: | Effective teamwork characteristics |

| |

Leadership should reflect the team’s stage of development and when leader’s delegate responsibility appropriately, team members become more confident and autonomous in their work.

Furthermore, it has also been revealed (Wingwon and Piriyakul, 2010a) that entrepreneurship and leadership of organizations have an indirect effect on an organization’s competitive advantage and financial performance. Leadership however has a higher effect over entrepreneurial skills. The study by Wingwon and Piriyakul (2010a) indicated that entrepreneurs must practice leadership without relying solely on charismatic personality traits as each entrepreneur has to drill and train their managerial skills, negotiation skills, decision making abilities along with the ability to pull employees together as a team.

This is consistent with the study of Matzler et al. (2008) ‘The relationship between transformational leadership, product innovation and performance in SMEs’ which the researchers found that leadership is the key role determining the strategic direction of the organization. This will result in innovative manufacturing and improved performance leading to its success and growth, including profits (Siriwoharn, 1997). They should also have the ability to modify and convince attitudes and behavior as well as sustain it, providing a stimulating environment in which task management and recognition stimulates workers and lower managers (Chairit, 2007).

Each organization will have a different structure which is dependent on the type, size and its configuration and functionality. It is the responsibility of each agency to facilitate efficient business operations (Martins and Terblanche, 2003; Blayse and Manley, 2004; Zazzali et al., 2008) and share responsibility for information and business decisions instead of being sourced from a single owner.

The ability to instill motivation by managers and executives and create a positive workplace environment instills the teams to greater heights which often times exceed the goals set (Chairit, 2007). This is consistent with theories of leadership reform.

Traditionally, doctors have been accorded and have assumed leadership of healthcare teams, regardless of their competence (Horwitz et al., 2011). However, new roles for healthcare leaders are emerging that incorporate team development, in order to maintain clinical productivity and patient satisfaction (Carr-Hill, 1992).

Investment: Major retailers, brand marketers and brand manufacturers have been stressing their desire to work with fewer, larger and more capable suppliers, strategically located around the world. In addition, there has been a consolidation among the lead firms, as the largest retailers (Walmart), traders (Li and Fung), brand marketers (Nike) and brand manufacturers (VF Corporation) are increasing their market shares through mergers, acquisitions and bankruptcies within the textile and apparel chain (Gereffi and Frederick, 2010).

Other conditions which affect operations are investment size, total number of staff, (OSMEP, 2013), equipment investment and tool technology. Machine technology and investment in its equipment is something that enhances the organization regardless of the size. Smaller companies investing in more sophisticated machine tools can enhance productivity, thus reducing their labor and contributing to better productivity (Joshi and Singh, 2010; Istook, 2000).

Wingwon and Piriyakul (2010b) stated that the organization that has a large competitive advantage will also have the ability to create a higher Return On Investment (ROI), as well as high business liquidity and a high market share. Additionally, the organization will have access to capital and material assets, creating an environment for sustainable investment size reducing the cost of production while creating a competitive advantage over its competitors. This in turn, creates more profitability including a higher return on investments.

Research on the Zimbabwe textile industry by Muranda (1999) showed that there is a positive correlation between firm size and present total investment in production for large firms. There is also a positive relationship between firm size and investments in production over a five year period among large companies. There is however no relationship among these variables in small and medium sized companies.

Research and Development (R and D): Karaveg (2013) revealed that most new products from small and medium sized enterprises (SMEs) in the Thai textile middle stream industry were products of incremental innovation which had low rates of R and D investment with limited numbers of skilled workers in science and technology. Another study studied the impact of degree of skills, favorable working environment and R and D on manufacturing productivity of labor-intensive industries. The study concluded that a higher degree of skills, favorable working environment and R and D are important inputs to a labor-intensive manufacturing process which is positively associated with productivity (Islam and Shazali, 2011).

Lower R and D time means faster time to market-critical to both the firm and its customers (Bhagwat, 2011).

Market orientation can have a positive relationship and determine the direction of organizational learning (Farrell, 2000), especially where the learning organization is continuously investing in R and D (Chongsung, 1991; Odagiri, 1983) while meeting appropriate market demands (Chen and Cheng, 2007) while contributing to the development of new products.

The European textile and clothing manufacturers are relocating to low cost areas where there is skilled labor. They are moving the source of competitiveness away from low cost, towards other more sophisticated factors, such as design, fashion, new fabrics and so forth. They invest heavily in research, development and in technology in order to produce new techniques of production which enable them to reduce the impact of labor cost (Stengg, 2001).

The difference in manufacturing processes is also important (Chen and Cheng, 2007), thus, the image, quality and the length of manufacturing process are supported. The learning organization is continuously investing in research and development (R and D) (Chongsung, 1991; Odagiri, 1983) leading to product development and innovation in new production processes to leading to the creation customer value-added products (Staritz, 2012).

This represents the changing nature of the product which has changed over time (Watchravesringkan et al., 2010). ‘Fast fashion’ is a concept where delivery times are short and organizations must move quickly to get their product from concept to customer. They therefore must develop innovative ways using technology to deliver goods quickly while keeping pace with market demands. E-commerce is one of these methods (Bae, 2005; Salam, 2005) and affects the growth of the organization (Odagiri, 1983).

Corporate strategy consists of research and development as well as branding which are all factors that make a difference in corporate strategy and are consistent with the theory contained in Michael E. Porter’s book “The five competitive forces that shape strategy” which has discussed product differentiation (Fig. 6). The corporation should present the product’s value by its identity and compete with rival firms’ product quality and after-sales services.

| |

| Fig. 6: | Porter’s 5 forces. Porter (2008) |

Competitiveness: The fashion industry has significantly evolved, particularly over the last 2 decades while te changing dynamics of the fashion industry has forced retailers to desire low cost and flexibility in design, quality and speed to market which are key strategies to maintaining a profitable position in the increasingly demanding and competitive market (Bhardwaj and Fairhurst, 2010).

Research by Salam (2005) suggested that the sources of competitive advantage are critical to a firm’s performance. This finding is in line with the extant literature stating in competitive industries, the more the resources, the better a firm will perform. The findings also revealed that the most critical set of the supply chain enablers contributing to firm performance is a combination of information technology capabilities and integration via competitive advantage. It was also demonstrated that firms need to incorporate supply chain orientation into their business strategy and supply chains should be an absolute core of a firm’s business model, in the competitive environment of the Thai garment industry.

According to research for the Serbian garment industry, researchers (Martinovic and Colovic, 2007) indicated that in today’s competitive market place, there is a need for business organizations to ensure continued improvement and garment manufacturing companies will experience growing pressure to improve quality, increase productivity and reduce cost with limited resources. The fashion industry will therefore need to reduce response times, eliminate errors and improve customer satisfaction.

According to Bhardwaj and Fairhurst (2010), “Fast Fashion” is a concept that will continue to affect the fashion apparel industry over the next decade and will have a direct effect on the way consumers purchase and react to trends. Although, continued research relative to the supply-side of fast fashion is important, emphasis should be placed on examining consumers’ perceptions of fast fashion. Empirical understanding of consumer characteristics and their motivation to make purchase decisions for throwaway fashion can help retailers in developing effective marketing strategies to perform more effectively in the market.

According to Moore and Fairhurst (2003), intense competition and short product life cycles in fashion retailing present a number of marketing challenges for retail firms in both the USA and abroad. In order to survive in this industry, it is vital for participants to develop and leverage core marketing capabilities with the most effective marketing capabilities, in terms of performance, being image differentiation and promotional capability.

This agrees with Watchravesringkan et al. (2010) who stated that the recent liberalization of the world’s textile and apparel trade policies and the consequent changes in trade patterns, poised threats to smaller textile and apparel exporting nations, including Thailand. Thus it is important to understand how the new trade environment affects the competitiveness of Thailand's apparel industry with findings revealing the existence of four determinants supporting the Thai apparel industry: Basic very specialized factors; sophisticated and demanding consumer market; the presence of interdependent economic agents and strategies and structure of Thai companies and domestic rivals. These four determinants are identical to the “Diamonds” outlined in Porter’s theory of “The competitive advantage of nations” (Porter, 1990) a new source of competitiveness (Fig. 7). Furthermore, the Thai government was found to play an important role, by providing support to enhance the global competitiveness of Thai companies.

For this study, Porter’s Diamond Model is used to analyze the effects of business environmental factors on business operation s and AEC competition (Fig. 7). With it, one can see the vast array of interrelationships within the industry and how these factors can affect competitiveness.

Even though the total global imports of textiles and clothing will expand, competition is also likely to increase among many garment exporting countries around the world. It is expected that textile and garment companies in medium-to high-cost countries will reduce their manufacturing production (Thephavong et al., 2014). In contrast, those in low-cost countries with a strong competitive advantage will expand their production and export capacities to become preferred suppliers and to take advantage of liberalization.

Creating a different image in the apparel and fashion industries is dependent on seasonal changes (Hopp, 2007).

| |

| Fig. 7: | Porter’s Diamond Model as applied to Thailand’s garment industry |

| |

| Fig. 8: | Conceptual Model of how investment, leadership, teamwork and R and D influence competitiveness of the Thai garment industry within the AEC |

Especially with garment products, as it is necessary for fashion products to have short delivery times with the shortest possible introduction times between new products from sellers to buyers (Chaudhry and Hodge, 2012).

From the above conceptual review and development, the researchers have developed the following nine hypotheses for the study (Fig. 8):

| • | Hypothesis 1 (H1): Leadership influences investment |

| • | Hypothesis 2 (H2): Leadership influences teamwork |

| • | Hypothesis 3 (H3): Leadership influences R and D |

| • | Hypothesis 4 (H4): Leadership influences competitiveness |

| • | Hypothesis 5 (H5): Investment influences R and D |

| • | Hypothesis 6 (H6): Teamwork influences competitiveness |

| • | Hypothesis 7 (H7): Teamwork influences R and D |

| • | Hypothesis 8 (H8): Teamwork influences competitiveness |

| • | Hypothesis 9 (H9): R and D influences competitiveness |

METHODOLOGY

Thai Garment Manufacturers Association’s executives were queried using quantitative research methods of which 178 responded to 289 inquiries.

| |

| Fig. 9: | 5-Point Likert Scale and range of mean score |

| |

| Fig. 10: | Sample size methodology. n: Sample size, N: No. in the research population, e: Error allowance of sample (0.05) |

The responses to the questions capturing focal constructs using a five-point Likert scale (Likert, 1970) with rating statements 1-5; 1 = Not at all important to 5 = Very important to survey questions such as “I am satisfied with the overall turnover of the firm” and “Your company’s net profit has increased compared to last year” under ‘Corporate/Business Performance’ (Fig. 9).

Data collection: Using Yamane (1973), sample size was calculated from a total Thai Garment Manufacturers Association membership population of 289 which resulted in the need of a minimum sample size of 74 to achieve an acceptable error rate (Fig. 10). This number however was exceeded considerably, as 178 members returned the survey to the researchers for this study.

The samples used in this study were to determine the appropriate sample size and to gain greater confidence with the survey questions. The research method used to calculate the sample size used the formula from Yamane (1973) at the 95% level of significance to calculate the size of the random sample.

The required sample size by using Yamane (1973) was 74 but researchers wishing to add higher confidence, collected and used data from 178 TGMA entrepreneurs in Thailand.

Additionally, qualitative research was conducted with in-depth interviews of 10 senior-level industry executives from Thailand’s top 10 ‘Business Success’ list.

Quantitative measurement: Competitiveness analysis of the Thai garment industry and its relationship with AEC used a measurement instrument or questionnaires utilizing a 5-Point Likert Scale (Likert, 1970).

Dependent variable: Competitiveness analysis of the Thai garment sector used a measurement instrument or questionnaires utilizing a 5-Point Likert Scale (Likert,1970) which were developed and constructed from scales enabling the measurement of Competitive Advantage, Cost Advantage and Customer Response (Bhardwaj and Fairhurst, 2010; Salam, 2005; Martinovic and Colovic, 2007; Moore and Fairhurst, 2003; Watchravesringkan et al., 2010; Porter, 1990; Thephavong et al., 2014; Hopp, 2007; Chaudhry and Hodge, 2012).

Independent variables: The scales for Leadership were developed using an analysis tool with a 5-point Likert scale (Likert, 1970) and have been constructed with two aspects (Table 2) including Management Experience (mannageexp) and Interpersonal Skill (Interskill) (Subramanian and Gopalakrishna, 2001; Asiegbu et al., 2012; Farrell, 2000; Barczak, 1996; Proctor-Childs et al., 1998; Wingwon and Piriyakul, 2010b; Matzler et al., 2008; Siriwoharn, 1997; Chairit, 2007; Martins and Terblanche, 2003; Blayse and Manley, 2004; Zazzali et al., 2008; Horwitz et al., 2011; Carr-Hill, 1992) The scales for Investment were developed using an analysis tool with a 5-Point Likert Scale query (Likert, 1970) and have been constructed with two aspects (Table 2) including Number of Employees (noofemployee) and Assets and Technology (Gereffi and Frederick, 2010; Joshi and Singh, 2010; Istook, 2000; Wingwon and Piriyakul, 2010b; Muranda, 1999).

| Table 2: | Statistic values presenting convergent validity of reflective scales of latent variables |

| |

The scales for Teamwork were developed using an analysis tool with a 5-Point Likert Scale query (Likert, 1970) and have been constructed with three aspects (Table 1) including Employee Participation (employpart), Communication (commu) and Incentive (incentive) (Katzenbach and Smith, 1993; Ducanis and Golin, 1979; Brannick et al., 1997; Hackman, 1990; West, 1994; Piriyakul, 2010; Keane and Te Velde, 2008; Ladda, 2012).

The scales for R and D (Research and Development) were developed using an analysis tool with a 5-Point Likert Scale query (Likert, 1970) and have been constructed with two aspects (Table 2) including Management Support (managesup) and Product and Process Innovation (proinno) (Karaveg, 2013; Islam and Shazali, 2011; Bhagwat, 2011; Farrell, 2000; Chongsung, 1991; Odagiri, 1983; Chen and Cheng, 2007; Staritz, 2012; Watchravesringkan et al., 2010; Bae, 2005; Salam, 2005).

RESEARCH ANALYSIS AND RESULTS

Partial Least Squares has been applied for analysis of quantitative data by the researcher. It is data analysis for Confirmatory Factor Analysis (CFA) relating to the determination of manifest variable and latent variable and testing of research hypothesis exhibiting in structural model analyzed by using the applications of PLS-Graph (Chin, 2001).

According to the analysis result of scale validity and reliability, scale investigation has been conducted using internal consistency measurement coefficient alpha. (α-coefficient) of Akron BAC (Cronbach) to calculate the average value of the correlation coefficient was found that alpha coefficients ranged from 0.606-0.905 which is considered to have high reliability.

In case of measure variables with reflective analysis, convergent validity has been conducted. Loading is used as consideration criteria and must be positive quantity and indicator loading has been more than 0.707 and all values have been statistically significant (|t|≥1.96) representing convergent validity of scales (Lauro and Vinzi, 2004; Henseler et al., 2009) quoted in Piriyakul (2010) and analysis results as shown in Table 2.

Investment (Investment) factors underlying the external variables are influenced by the Number of Employees (noofemployee) and Assets and Technology (assetntech) with values loading from 0.707 and a significant level of confidence percentage 95 (t-stat>1.96) which considers such factors highly reliable. These factors have a direct and positive impact on R and D and Competitiveness as shown in Fig. 11.

Leadership (leadership) factors underlying the external variables are influenced by Management Experience (manageexp) and Interpersonal Skill (interskill) with values loading from 0.707 and a significant level of confidence percentage 95 (t-stat>1.96) which considers such factors highly reliable. These factors have a direct and positive impact on Investment, Teamwork and Competitiveness while having minimum effect on R and D as shown in Fig. 11.

Teamwork (Teamwork) factors underlying the external variables are influenced by Employee Participation (employpart), Communication (commu) and Incentive (incentive) with values loading from 0.707 and a significant level of confidence percentage 95 (t-stat>1.96) which considers such factors highly reliable. These factors have a direct and positive impact on R and D but have minimal effect on Competitiveness as shown in Fig. 11.

R and D (RD) factors underlying the external variables are influenced by Management Support (managesup) and Product and Process Innovation (proinno) with values loading from 0.707 and a significant level of confidence percentage 95 (t-stat>1.96) which considers such factors highly reliable which has a direct and positive influence on Competitiveness as shown in Fig. 11.

| |

| Fig. 11: | Final model-analysis of factors that affect Thai garment industry competitiveness within the AEC |

Competitiveness (Competitiveness) factors underlying the external variables are influenced by three aspects including Competitive Advantage (competadv), Cost Advantage (costadv) and Customer Response (custres) with values loading from 0.707 and a significant level of confidence percentage 95 (t-stat>1.96) (Fig. 11) which considers such factors highly reliable.

The above reflective model in Table 2 shows the discriminant validity of the internal latent variables and the correlation of variables. It also depicts the scale reliability which has been analyzed from Composite Reliability (CR) as well as the Average Variance Extracted (AVE) and R2. The CR value should not go below 0.60 and the AVE values should also drop below 0.50 and R2 values should not be under 0.20 (Lauro and Vinzi, 2004; Henseler et al., 2009) quoted by Wingwon and Piriyakul (2010a).

Table 3 below shows the results of factor analysis affecting the Thai garment industry competitiveness. The data also shows the CR values are higher than 0.60, with all AEV values higher than 0.50 for all values and R2 values higher than 0.20, representing the reliability of the measurement. It found that data sets in the ![]() have higher values than all of the corresponding values in the ‘Cross Construct Correlation’ in the same column, representing discriminant validity of the measure in each construct and with a greater value than 0.50 of AVE as shown in Table 3. The samples were analyzed to answer the research hypotheses criteria in the nine assumptions presented in Table 4.

have higher values than all of the corresponding values in the ‘Cross Construct Correlation’ in the same column, representing discriminant validity of the measure in each construct and with a greater value than 0.50 of AVE as shown in Table 3. The samples were analyzed to answer the research hypotheses criteria in the nine assumptions presented in Table 4.

| Table 3: | Confirmatory Factor Analysis (CFA) of the independent variables of leadership, investment, teamwork and R and D and their effects on the dependent variable of competitiveness |

| |

| CR: Composite reliability, R2: Square of the correlation, AVE: Average variance extracted. Statistical significance level is at 0.01 and diagonal figures mean | |

| Table 4: | Research hypotheses test results |

| |

| *,** At the 90 and 95% confidence level, respectively. Coefficient refers to the Beta (β). t-stat is the t-value | |

Furthermore, the structural analysis model framework was used to research the t-test coefficients and their relationship of each path of the t-test hypothesis with significance greater than 1.96. This explains the results obtained from analysis as shown in Table 2 and 3 as well as the test results presented in Table 4.

CONCLUSION

The study of ‘AEC Garment Industry Competitiveness: A Structural Equation Model of Thailand’s Role’ has so far found that Thailand is clearly losing the competitive battle to its AEC neighbors, primarily due to the governmental mandated rise in labor costs to 300 baht day-1. This has therefor led to an exodus of larger enterprises to CLMV countries where labor is less expensive while many smaller Thai garment SMEs have ceased operations. The study however does provide a window into how Thailand’s garment institutions need to embrace research and development thereby raising the international image and competitiveness of its apparel products. Additionally, leadership and workforce teamwork are key components which affect the industry’s future success. Additionally, Thailand’s garment and textile industry is highly labor intensive and larger organizations have a significantly higher contribution factor to the industry’s growth. A key component of this analysis determined that R and D, investment and leadership were also key factors in maximizing influences and competitiveness of the Thai Garment Industry.

REFERENCES

- Blayse, A.M. and K. Manley, 2004. Key influences on construction innovation. Constr. Innovation Inform. Process Manage., 4: 143-154.

CrossRef - Karaveg, C., 2013. Factors affecting the innovation capacity of Thai textile and clothing industries in Thailand. Int. J. Res. Manage. Technol., 3: 37-42.

Direct Link - Christopher, M., R. Lowson and H. Peck, 2004. Creating agile supply chains in the fashion industry. Int. J. Retail Distrib. Manage., 32: 367-376.

CrossRef - Istook, C.L., 2000. Rapid prototyping in the textile and apparel industry: A pilot project. J. Text. Apparel Technol. Manage., 1: 1-14.

Direct Link - Chaudhry, H. and G. Hodge, 2012. Postponement and supply chain structure: Cases from the textile and apparel industry. J. Fashion Marketing Manage., 16: 64-80.

CrossRefDirect Link - Henseler, J., C.M. Ringle and R.R. Sinkovics, 2009. The Use of Partial Least Squares Path Modeling in International Marketing. In: New Challenges to International Marketing (Advances in International Marketing, Volume 20), Cavusgil, T., R.R. Sinkovics and P.N. Ghauri (Eds.). Emerald Group Publishing Ltd., Bingley, UK., ISBN-13: 978-1848554689, pp: 277-319.

- Joshi, R.N. and S.P. Singh, 2010. Estimation of total factor productivity in the Indian garment industry. J. Fashion Marketing Manage., 14: 145-160.

CrossRefDirect Link - Watchravesringkan, K., E. Karpova, N.N. Hodges and R. Copeland, 2010. The competitive position of Thailand's apparel industry: Challenges and opportunities for globalization. J. Fashion Marketing Manage., 14: 576-597.

CrossRefDirect Link - Moore, M. and A. Fairhurst, 2003. Marketing capabilities and firm performance in fashion retailing. J. Fashion Marketing Manag., 7: 386-397.

CrossRefDirect Link - Farrell, M.A., 2000. Developing a market-oriented learning organisation. Aust. J. Manage., 25: 201-223.

CrossRefDirect Link - Martins, E.C. and F. Terblanche, 2003. Building organisational culture that stimulates creativity and innovation. Eur. J. Innov. Manage., 6: 64-74.

CrossRefDirect Link - Porter, M.E., 2008. The five competitive forces that shape strategy. Harv. Bus. Rev., 86: 78-93.

PubMed - Piriyakul, M., 2010. Partial least square path modeling (PLS path modeling). Proceedings of the 11th Academic Conference of Applied Statistics, November 19-20, 2010, Bucharest, Romania.

Direct Link - Muranda, Z., 1999. xport entry decision and organizational characteristics of textile and clothing export firms: Analysis of Zimbabwean firms. Zambezia, 26: 183-209.

Direct Link - Odagiri, H., 1983. R & D expenditures, royalty payments and sales growth in Japanese manufacturing corporations. J. Ind. Econ., 32: 61-71.

Direct Link - Subramanian, R. and P. Gopalakrishna, 2001. The market orientation-performance relationship in the context of a developing economy: An empirical analysis. J. Bus. Res., 53: 1-13.

CrossRefDirect Link - Islam, S. and S.T.S. Shazali, 2011. Determinants of manufacturing productivity: Pilot study on labor-intensive industries. Int. J. Prod. Perform. Manage., 60: 567-582.

CrossRefDirect Link - Thailand Environment Institute, 2003. Thailand case study on environmental requirements, market access and competitiveness in the leather and footwear sectors. Proceedings of the Sub-Regional Workshop on Environmental Requirements, Market Access/Penetration and Export Competitiveness for Leather and Footwear, November 19-21, 2003, Bangkok, Thailand.

- Bhardwaj, V. and A. Fairhurst, 2010. Fast fashion: Response to changes in the fashion industry. Int. Rev. Retailing Distrib. Consum. Res., 20: 165-173.

CrossRef - Wingwon, B. and M. Piriyakul, 2010. Determinant of entrepreneurship, leadership, technology and guanxi of small and medium enterprises in Northern region of Thailand. Proceedings of the Annual National Conference of National Higher Educational Academic Research Networking, May 27, 2010, Khon Kaen University, Khon Kaen Province.

- Zazzali, J.L., C. Sherbourne, K.E. Hoagwood, D. Greene, M.F. Bigley and T.L. Sexton, 2008. The adoption and implementation of an evidence based practice in child and family mental health services organizations: A pilot study of functional family therapy in New York State. Admin. Policy Mental Health Mental Health Serv. Res., 35: 38-49.

CrossRefPubMedDirect Link - Wingwon, B. and M. Piriyakul, 2010. Antecedents of PLS path model for competitive advantage and financial performance of SMEs in Thailand. Afr. J. Market. Manage., 2: 123-135.

Direct Link - Carr-Hill, R.A., 1992. The measurement of patient satisfaction. J. Public Health Med., 14: 236-249.

PubMed - Horwitz, I.B., M. Sonilal and S.K. Horwitz, 2011. Improving health care quality through culturally competent physicians: Leadership and organizational diversity training. J. Healthcare Leadership, 3: 29-40.

CrossRefDirect Link - Martinovic, M. and G. Colovic, 2007. System PPORF in garment industry. Serbian J. Manage., 2: 77-85.

Direct Link - Proctor-Childs, T., M. Freeman and C. Miller, 1998. Visions of teamwork: The realities of an interdisciplinary approach. Br. J. Therapy Rehabil., 5: 616-635.

Direct Link