Natthapat Teeranantawanichand

Administration and Management College, King Mongkut�s Institute of Technology Ladkrabang, Thailand

Wanno Fongsuwan

Administration and Management College, King Mongkut�s Institute of Technology Ladkrabang, Thailand

Research Journal of Business Management

Year: 2014 | Volume: 8 | Issue: 4 | Page No.: 538-551

ABSTRACT

This study was undertaken to study the factors that affects foreign leasing and ownership of real estate holdings in Thailand’s ‘Special Autonomous Systems’ (SAS) located within the Bangkok metropolitan area as well as the coastal resort city of Pattaya situated along a 15 km stretch of the Gulf of Thailand’s eastern shore. In 2012, Bangkok was once again ranked 1st as the ‘World’s Best City’ while Pattaya has grown from a tiny fishing village 2 h southeast of Bangkok to what some estimate is a half million people during the height of the tourist season. As the regional air, transportation and logistics hub of Southeast Asia, Bangkok’s role within the AEC can’t be underestimated. Pattaya, whose average beachfront land has trebled in the past 10 years, has become the place to visit and live for both Thais and foreigners. Thai government authorities are projecting 10 million visitors for Pattaya in 2015, with US $3.26 billion in tourism receipts. Additionally, between 2008-2013 Bangkok in some areas saw a 150% jump in commercial property values. Results of this study found that government policy has a direct and positive effect on the economy and investment as well as the types of foreign real estate holdings types. Additionally, the economy and investment had a direct and positive influence on foreign real estate holdings.

PDF Abstract XML References Citation

Received: January 11, 2014;

Accepted: April 27, 2014;

Published: June 23, 2014

How to cite this article

Natthapat Teeranantawanichand and Wanno Fongsuwan, 2014. Foreign Real Estate Holdings in Thailand’s

Special Autonomous Systems (SAS) Bangkok and Pattaya: A Structural Equation

Model. Research Journal of Business Management, 8: 538-551.

DOI: 10.3923/rjbm.2014.538.551

URL: https://scialert.net/abstract/?doi=rjbm.2014.538.551

DOI: 10.3923/rjbm.2014.538.551

URL: https://scialert.net/abstract/?doi=rjbm.2014.538.551

INTRODUCTION

Despite internal and ongoing political tensions and severe flooding in 2011, Thailand continues to maintain an open market-oriented economy and encourages foreign direct investment as a means of promoting economic development, employment and technology transfer. In recent decades, Thailand has been a major destination for foreign direct investment. Thailand continues to welcome investment from all countries and seeks to avoid dependence on any one country as a source of investment.

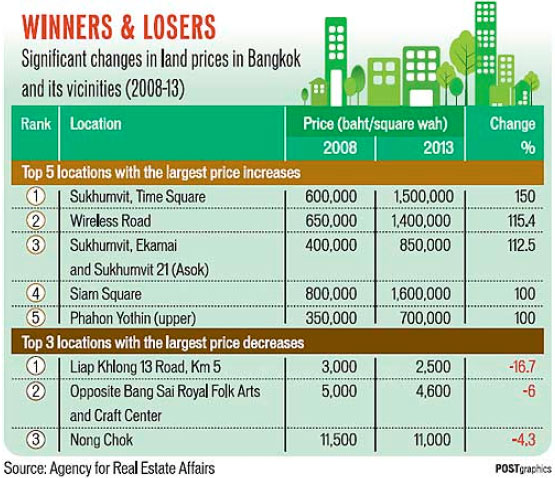

Understanding the history, attraction and strategic location of both Bangkok and Pattaya is important to understanding, why foreigners have been a key to these areas spectacular growth in foreign real estate holdings. Along with this, are factors concerning the economy and investment as well as government policy impacting foreign FDI with Bangkok in 2012 being ranked first in the Travel and Leisure magazine’s online survey of the world’s best cities (Fig. 1) (TLM, 2013).

According to the Chonburi Provincial Administration Organization, which oversees tourism development in Pattaya, in 2015 Pattaya is projected to have 10 million international and domestic visitors with a US $3.26 billion infusion into the local economy.

| |

| Fig. 1: | Bangkok land prices 2008-2013, Source: Agency for Real Estate Affairs 2014 |

Historically, figures from Thailand's Ministry of tourism and sports, Pattaya received 8.3 million arrivals in 2010, which was a 93% jump over 2009. For the period January-June 2011, there were 724,273 Thai and 3,070,635 foreign visitors to Pattaya (WPC, 2012).

Pattaya city has been administered under a special autonomous system since 1978. It has a status comparable to a municipality and is separately administered by the mayor of Pattaya city, who is responsible for making policies, organizing public services and supervising all employees of Pattaya city administration.

Bangkok was given special status in 1972, when it became a province but retained its powers as a thesaban (municipality). Pattaya was given special status in 1978 as a distinct urban area due to its status as a tourist destination. Until 1998, Bangkok and Pattaya commanded like thesaban, weak authoritative competences due to central control. The Decentralization Act of 1999 gave thesaban and tambon and hence, also Bangkok and Pattaya, specific policy competences with relatively large budgets (TCP, 2007). These policy competences extend beyond the largely infrastructure-oriented tasks and projects of the changwat with Bangkok reflecting the aggregate changwat and municipal competences-but without residual powers or control over institutional set-up or police. Pattaya, reflecting only the municipal increase rather than the aggregate provincial and municipal powers of Bangkok is somewhat weaker than that of the Bangkok municipality (TCP, 2007).

Thailand however is still a developing country with Foreign Direct Investment (FDI) a crucial component of this growth but the continuing political crisis has depressed the average increase in Greater Bangkok land prices in 2014. This has been due to government spending delays according to Thailand’s Agency for Real Estate Affairs (AREA), which stated that growth in land prices for Bangkok and the vicinity in 2014 are only estimated at 3% or lower, which is the lowest since 2010 (AREA, 2014).

With the military coup d'état in late May 2014, direct investment in Thailand was stated by the vice-chairman of the Joint Foreign Chambers of Commerce in Thailand as having the potential to “take a big hit” (Bangkok Post, 2014a). Additional data released by Thailand’s Board of Investment (BoI) only one day after the coup seemed to support this sentiment indicating that of the 399 projects submitted for investment incentives in the first four months of 2014, the figures were down 42% year-on-year, with total investment value falling 44.8% to 270 billion baht due to the many months long political standoff. Additionally, investments from Japan, Thailand’s top foreign investor, fell 41% from 216 projects last year, with investment value also sliding 55% from 150 billion baht (Bangkok Post, 2014a).

This is in contrast to land prices rising every year since 2000 in Bangkok. Between 2008-2013 Bangkok in some areas saw a 150% jump in commercial property values (AREA, 2014). During the past 10 years, the lowest increase was in chaotic 2009 (2.9%) while the average yearly increase during 2004-2013 was 4.4% Bangkok Post (2014b). Additionally, for 2014, AREA forecasts that the value of project launches in Bangkok and its suburbs will drop by 30-40% from last year's Bt385 billion. In the Bangkok metro area, only 30 residential projects totaling 4,438 units worth Bt15.63 billion were launched in December 2013. That was a decline from November 2013 of 30% in terms of projects, 73% in terms of units and 69% in terms of value, according to a survey by the Agency for Real Estate Affairs (The Nation, 2014).

The highest land prices in 2013 were once again in Siam Center, Chidlom and Phloenchit (all land in the Siam Center area is leasehold) at 1.65 million baht per square wah (4 square meters). These three locations were followed by Siam Square (1.6 million baht per 4 square meters), where all land is leasehold. The lowest land prices in Greater Bangkok were along Liap Khlong 13 Road at 5 km in the Lam Luk Ka area of Pathum Thani (2,500 baht per sq wah), a location quite far from the capital with insufficient facilities and roads. Among 10 locations along current and future mass transit lines, the highest increase in average land prices last year was along the Blue Line between Bang Sue and Tha Phra at 12.8%. The average increase in the 10 locations was 8.9% (Bangkok Post, 2014b).

Additionally, according to Thailand’s Home Builder Association, along with the healthy growth in land prices was the additional supply of 705,000 new condominiums in 2013 into the market, the highest record ever in the industry’s history (Thai PBS, 2013). According to Bank of Thailand statistics, condo prices in Q1 2013 soared by 9.39%, while townhouses prices rose by 6.86%, after rising by similar amounts for the past several years. Total transactions by value, including land and buildings, surged 35.3% in Q1 2013 as total outstanding property credits rose by 13.3% (Forbes, 2013).

As can be seen from this study’s data, the motivation for a high potential return on a real estate transaction investment in both Bangkok and Pattaya has been large, but political turmoil and risk has entered into the equation. The mechanism however, in which these transactions take place by foreigners in Thailand take on various forms due to the uniqueness of Thailand’s laws. This can include purchasing, renting, nominees, investment or corporate. Relevant factors include economy and investment, which are variables related to the cost and difficulty of investing. This also includes the economic situation, including interest rates, which is related to the Return On Investment (ROI) and patterns of international investment. Other factors include government policy, promotion and governmental support which also include financing, taxes and legal transparency. The above factors all affect the desire and intent to hold real estate in Thailand by foreigners.

This intent can take many indirect forms however, as land ownership in general for non-Thai businesses and citizens are not permitted to own land in Thailand unless the land is on government-approved industrial estates. Under the 1999 amendment to the Land Code Act, foreigners who invest a minimum of 40 million Baht (approximately US$1.3 million) are permitted to buy up to 1,600 square meters (1 rai) of land for residential use with the permission of the Ministry of Interior. If the required land is not used as a residence within two years from the date of acquisition and registration, the Ministry has the power to dispose of the land (US DoS, 2012).

Petroleum concessionaires may own land necessary for their activities. Rather than purchasing, many foreign businesses instead sign long-term leases and then construct buildings on the leased land. Under the 1999 Condominium Act, non-Thais were allowed to own up to 100% of a condominium building if they purchased the unit between April 28, 1999 and April 28, 2004. Under the newer Condominium Act of 2007, foreign ownership in a condominium building, when added together, must not exceed 49% of the total space of all units in the building, except for those purchased between 1999 and 2004 (US DoS, 2012).

The use of such property in any form depends on several factors. One factor includes the environment which includes the condition and appearance of the real estate. Another includes land use, which can include zoning, which helps maximize benefits of the land itself.

Thus to exploit its full potential, Thailand’s Board of Investment (BoI) was established to promote investments to investors in both Thailand and to foreigners with a mission to increase the competitiveness and facilitate investment. BOI’s business support services provide information and advice about setting up a business in Thailand, management visits to study the suitability of plant locations, manufacturer’s supply parts OEM and partnerships, contact details of agencies, both public and private. Additionally, coordinate and cooperate with foreign businesses and other government agencies including marketing to promote Thailand as a source of support as one of the best investments in Asia. It also is assigned to prepare and implement strategic plans, which define and influence the global investment activities throughout the year.

Investments are both direct and indirect, with direct taking the form of real-estate holdings allocated for the production of goods and services. Indirect investment is obtained through the trading of financial securities. The investment model depends on the purpose of the investment.

In addition, in today's globalized world where investments flow freely and the integration of economic, social and political agreements formalize these movements, whereas trading blocs such as the ASEAN Economic Community (AEC) become crucial to these processes.

The three pillars of the ASEAN community, namely the ASEAN Political-Security Community (APSC), the ASEAN Economic Community (AEC) and the ASEAN Socio-Cultural Community (ASCC), are the most crucial areas deemed necessary for the progress and evolution of ASEAN and its peoples. The Blueprints of these three communities have been carefully formulated to detail specific strategic objectives and actions which intend to achieve progress and positive development in the respective areas (Keng, 2009).

The AEC as one of the three pillars helps investors recognize the benefits of investing in the AEC with its beneficial conditions of participation and investment exchange between member nations. This will lead to higher investment in Thailand from foreigners, including the purchase of property, both in real estate and other sectors such as securities.

Investments affect Thailand’s economy and society and with these further investments, come a proportional increase in property holdings by foreigners but these real estate investments take on many forms.

Research from Satjanon et al. (2009) has said that the foreign use and possession of property in Thailand has occurred in a legal way but Thai people have been used as nominees to and in a way that the people of Thailand as holding legal title. But in practice these nominees, often times exploited and occupied by foreigners which impacts both positive and negative ways. It is imperative that Thailand manages and uses property in a systematic way.

The Thailand Development Research Institute (TDRI) also conducted a study and prepared a report on strategic land management which included the planning, land holdings, reserves and undeveloped land and reserved or restricted land. Consequently, this data has been utilized in drafting overall strategic management of land and land holdings and the governmental legislation pertaining to this as well as the holdings of land and property by foreigners.

It also has a created a special department which is unique to Thailand’s administration structure which provides an organization that manages and conducts local public services in the area that has some characteristics different from other areas of the country.

The authority of this organization is different from other organizations, such as in the areas of personnel and revenue management. In both Bangkok and Pattaya with their large numbers of foreigners, the researchers therefore wanted to undertake a study that investigated the variables of the implementation and the factors of these ‘Special Autonomous Systems’ of Thailand. Therefore, the researchers have conducted research of ‘Foreign Real Estate Holdings in Thailand’s Special Autonomous Systems (SAS) Bangkok and Pattaya a structural equation model’.

CONCEPTUAL DEVELOPMENT

Real estate holdings types: Real estate holdings of individuals have different purposes including residential and home as well as for career and professional reasons. Decisions affecting real estate holdings are very dependent on consumer behavior, which is associated with emotional behavior affecting the acquisition, the property’s use and decision to leave. Consumers steps in deciding to buy property are problems, data collection, evaluate alternatives, decision/ purchase behavior and after decision to purchase behavior (Rungruangphon, 2008).

Real estate holdings can be classified either as a purchase or a lease, but the decision to purchase or lease affects overall costs as purchasing increases debt load while renting decreases or significantly reduces the cost of the enterprise (Dowden and Humphreys, 2013).

Another form of ownership of real estate is that of the agent or nominee, which is an instrument used by a foreign entity to purchase land (Tan, 2004) or establish a corporation (Satjanon et al. 2009)

However, the factors that influence real estate holdings take many forms, such as the government policy to promote the use of land (Mohd et al., 2009), which are associated with legal factors, land ownership regulations (Camilleri, 2011) and factors of investment characteristics (Lopez et al., 1988) and whether investment are direct or indirect.

Investors need to consider both the opportunities available and the purpose of the investment. such as the selection of a location in which the objectives are different for residential and business purposes. If an investment is to be used for internal factors such as business expansion (expansion, new business, joint ventures with local entrepreneurs), the cost-effectiveness (cost of raw materials, labor, logistics and land rental) and size of business. (Investment capital and number of workers) and external factors, including the attitude of society, infrastructure, tax incentives and maintaining consistency with social attitudes, tax benefits and provincial strategies (Suttapong et al., 2010).

Economy and investment: Economic growth in developing countries requires continued investment and for developing countries, the investment from abroad is considered a critical factor for growth. Its benefits include the transfer of company knowledge and technology, including financial assistance and knowledge transfer to the country of investment. This also increases wages for worked in the manufacturing sector, which has a ‘knock-on’ affect for other benefits and domestic workers. Thus, the liberalization of foreign investments is important.

In a US land holdings research, the study conducted by Adelaja et al. (2010), it was discovered that there is an inverse relationship between the rate of land value appreciation and the demand for land by farmers. In the data from 48 states, spanning from 1950-2004, it was noted that government policies can trigger increases in the rate of appreciation of farmland which may also potentially result in the agricultural hoarding of land. Additionally, enhanced profitability in agriculture due to government programs targeting viability, commodity price support and reduction of regulation or market expansion programs can also potentially affect land retention.

And in the current era of globalization with its ability to move funds freely, policies and strategies must be considered carefully which makes Thailand a net benefactor of foreign investment.

Research from the OSMEP (2012) found that the factors that foreign investors take into consideration for investment are many but include market expansion, investors to create business, security and confidence of investment and no risk in finding new buyers. A reason to invest in overseas business is the ability to source cheap labor, ready manufacturing supply chains, productivity and ability to expatriate your capital investment, cheap resource materials and the ability to easily sell you product into the local market (Ratniyom, 2013).

Free Trade Agreements allow decisions to invest in property (Omran and Pointon, 2009) which results in many groups in many countries to trade between each other, taking advantage of production, products and services of the same type or not.

While has embraced the theory of imperfect competition to describe the emergence of international trade in a world of imperfect competition, international trade is driven as much by increasing returns and external economies as by competitive advantage. Furthermore, these external economies are more likely to be realized at the local and regional scale than at the national or international level. While Intra-Industry Trade is primarily a product in the same industry, there may be a difference in the product. Differential products, which is the difference of the product, will allow consumers to choose the product to be consumed from many different channels, allowing the consumer to, ‘diversity’ even more and ‘gain from variety’ itself.

In order to contribute to confidence in economic integration and greater prospects for agreements and trade within the region, there needs to be an agreement between the different areas of concern. Within the ASEAN community, the 7th AFAS package agreed to the following (Dee, 2013):

| • | To enhance cooperation in services amongst Member States in order to improve the efficiency and competitiveness, diversify production capacity and supply and distribution of services of their service suppliers within and outside ASEAN |

| • | To eliminate substantially restrictions to trade in services amongst Member States |

| • | To liberalize trade in services by expanding the depth and scope of liberalisation beyond those undertaken by Member States under the GATS with the aim to realising a free trade area in services |

Under the concept of trade liberalization between member states and ‘trade in services’, real estate services was also included with ASEAN investors being allowed to hold shares of not less than 70% by the year 2015.

However, members agreed that the option activity under the Central Product Classification or CPC, CPC 8210 (Real estate services Involving own or leased property) and CPC 8220 (Real estate services on a fee or contract basis) contain only one activity which is a commitment to open markets and it is achieved in the AEC blueprint in the field of real estate. Certain AEC countries such as Thailand, the Philippines and Singapore are ready for liberalization in their property and real sector while other ASEAN countries may not be ready and need to revert to their local investment laws for real estate investment (United Nations, 1991).

Government policy: The Thai government has formulated a policy to encourage investment which is established by the Board of Investment (BOI) to enhance competitiveness and facilitate investment and conduct business support services. The government also needs to determine monetary and fiscal including the various policies that can meet the goals of the provincial governments.

Research by Kasikorn Research Center (2012) found that government policy measures set a credit limit, conduct land appraisal, create tax incentives for the purchase of housing, legal processes for land ownership which all affects the real estate business direction and affect state policy related to trade and foreign investment.

As mentioned above, research shows that government policy measures to support investment require a combination of several measures, including measures to limit credit or financial measures that affect their access to capital. Financing advantages affecting investment decisions.

Research from Suttapong et al. (2010) stated that investor investment strategy would affect strategic mergers or acquisitions and the potential development of the company (Cohen, 2010) because the amount of financial sector support affects the real estate pricing models and helps in the decision to purchase the property faster and creates cash flow to market real estate (Roubi and Ghazaly, 2007).

Tax incentives measures, such as tax rates and associated fees, will affect land and buildings cost (Adelaja et al., 2010). If tax rates and fees are low and property prices also not high, businesses will be more lucrative contributing to increased production into the market. Having adequate amounts of real estate in the market will affect real estate prices and their purchase decision (Chan and Chen, 2011).

Real estate and property laws are determined by government regulations and zoning, such as with the textile industry which needs to be located near water (Ratniyom, 2013) and is considered the economic laws in force planning, financial systems related to credit (Mohd et al., 2009) the provisions of legal and legal environment of business operations is a major problem in India (Suttapong et al., 2010).

| |

| Fig. 2: | Final model-analysis of factors that affect types of real estate holdings within Thailand’s Special Autonomous Systems (SASs) |

From the above conceptual review and development, the researchers have developed the following three hypotheses for this study on Foreign Real Estate Holdings Types within Thailand’s Special Autonomous Systems (SASs) (Fig. 2):

| • | Hypothesis 1 (H1): Economy and investment have a direct and positive influence on the types of Real Estate Holdings |

| • | Hypothesis 2 (H2): Government policy has a direct and positive influence on the Types of Real Estate Holdings |

| • | Hypothesis 3 (H3): Government policy has a direct and positive influence on the economy and investment |

METHODOLOGY

Data collection: This study was conducted from a sample population of foreigners in the SAS areas of Bangkok and Pattaya City as well as from 10 executives from large, international organizations and Thailand’s Investment Promotion Agency using both quantitative and qualitative research, respectively.

Data collection: Quantitative research was conducted with Stratified Sampling by dividing the sample according to the pattern of land ownership, buyers, renters, nominees, corporations and investments held in the form of joint ventures. For this research, the measurement instrument or questionnaires utilized were prepared from the literature. A seven-point rating scale was employed for this survey.

Questionnaire design: For this research, the measurement instrument or questionnaires to be utilized were prepared from the literature. Quality and content was monitored with tools used in the research and as a measurement of quality. Both content validity and reliability was assured by 5 experts in their respective fields with an evaluation index consistent with the content and the purpose of the research (index of Item-Objective Congruence (IOC) to carry out screening questions specifically dealing with an IOC higher than 0.5 only. The selected items were dealt with using an IOC higher than 0.5. Questions were then rated by the use of the Likert rating scale with each class of measurements using a 7 unit scale for measuring internal consistency with coefficient (α-coefficient) of Akron BAC (Cronbach) to calculate for the average value of the correlation coefficient.

For this study, the measurement instrument or questionnaires utilized were prepared from the literature. To gauge both the content validity and reliability of the survey, 5 specialists in their respective fields were chosen to evaluate the consistency of the content and confirm it was valid for the purposes of the research. Additionally, the index of Item-Objective Congruence (IOC) developed by Rovinelli and Hambleton (1977) was employed to carry out the screening of questions. The IOC is a procedure used in test development for evaluating content validity at the item development stage. This measure is limited to the assessment of unidimensional items or items that measure specified composites of skills. The method prescribed by Rovinelli and Hambleton (1977) results in indices of item congruence in which experts rate the match between an item and several constructs assuming that the item taps only one of the constructs which is unbeknownst to the experts. The research then proceeded to select items that with an IOC index higher than 0.5 which were considered acceptable.

Questionnaires were constructed to be a tool to measure concept definition and practice. The instrument or questionnaire used the 7-Point (Likert, 1972) as the measurement scale and the conceptual framework for determining the internal consistency measured by coefficient alpha (α-coefficient) of Akron BAC (Cronbach) to calculate the average value of the correlation coefficient. All values lower than 0.50 were eliminated from the measurement. Qualitative research was collected from information from the executives of large international organizations and executives from Thailand’s Investment Promotion Agency in order to confirm the model of quantitative research with a sample of 10 executives selected for sampling using non-probability sampling using random sampling (purposive sampling).

Measurement

Dependent variable: Real Estate Holdings Types (Behav_ten) analysis used as a measurement instrument or questionnaire utilizing a 7-Point (Likert, 1972) and was constructed with the scales developed enabling measurement of Purchasing (Type_te1) and Long-Term Lease (Type_te3) (Satjanon et al., 2009; Rungruangphon, 2008; Dowden and Humphreys, 2013; Tan, 2004).

Independent variables: Economy and Investment (Econ_invest) analysis used as a measurement instrument or questionnaire a 7-Point (Likert, 1972) and was constructed with the scales developed enabling measurement of economy (Economics), interest rates (Interest) and foreign investment type (Invest_type) (Lopez et al., 1988; Suttapong et al., 2010; Adelaja et al., 2010; OSMEP, 2012; Ratniyom, 2013; Omran and Pointon, 2009; Kasikorn Research Center, 2012).

Government policy (Gov_policy) analysis used as a measurement instrument or questionnaire a 7-Point (Likert, 1972) and was constructed with the scales developed enabling measurement of financial incentives (Money_factor), tax incentives (Tax_factor) and legal transparency (Law_factor) (Mohd et al., 2009; Camilleri, 2011; Suttapong et al., 2010; Kasikorn Research Center, 2012; Suttapong et al., 2010; Cohen, 2010; Roubi and Ghazaly, 2007; Adelaja et al., 2010; Chan and Chen, 2011; Ratniyom, 2013; Suttapong et al., 2010).

RESEARCH ANALYSIS AND RESULTS

Partial Least Squares has been applied for analysis of quantitative data by the researcher. It is data analysis for Confirmatory Factor Analysis (CFA) relating to the determination of manifest variable and latent variable and testing of research hypothesis exhibiting in structural model analyzed by using the applications of PLS-Graph (Chin, 2001). According to the analysis result of scale validity and reliability, scale investigation was conducted using internal consistency measurement coefficient alpha (α-coefficient) of Akron BAC (Cronbach) to calculate the average value of the correlation coefficient, whose range was found to be highly reliable.

In case of measure variables with reflective analysis, convergent validity has been conducted. Loading is used as consideration criteria and must be positive quantity and indicator loading has been more than 0.707 and all values have been statistically significant (|t|≥1.96) representing convergent validity of scales (Lauro and Vinzi, 2004; Henseler et al., 2009) quoted in (Piriyakul and Wingwon, 2010) and analysis results as shown in Table 1.

Economy and investment (Econ_invest) factors underlying the external variables influencing economics (Economics), interest rates (Interest) and foreign investment type (Invest_type) with values loading from 0.707 and a significant level of confidence percentage 95 (t-. stat>1.96), which considers such factors highly reliable. It has a direct impact on Real Estate Holding types.

Government policy (Gov_policy) factors underlying the external variables influencing financial incentives (Money_factor), tax incentives (Tax_factor) and legal transparency (Law_facotr) with values loading from 0.707 and a significant level of confidence percentage 95 (t-stat>1.96), which considers such factors highly reliable. It has a direct impact on Economy and Investment and Real Estate Holdings Types.

Real Estate Holding types (Behav_ten) factors underlying the external variables influencing Purchasing (type_te1) and Long-Term Lease (Type_te3) with values loading from 0.707 and a significant level of confidence percentage 95 (t-stat>1.96), which considers such factors highly reliable.

The above reflective model in Table 1 shows the discriminant validity of the internal latent variables and the correlation of variables. It also depicts the scale reliability which has been analyzed from Composite Reliability (CR) as well as the Average Variance Extracted (AVE) and R2. The CR value should not go below 0.60 and the AVE values should also drop below 0.50 and R2 values should not be under 0.20 (Lauro and Vinzi, 2004; Henseler et al., 2009) quoted in Piriyakul and Wingwon, (2010).

| Table 1: | Statistic values presenting convergent validity of reflective scales of latent variables |

| |

| Table 2: | Confirmatory Factor Analysis (CFA) of the independent variables of economy and investment, government policy, social and environmental conditions on the dependent variable of real estate holdings types |

| |

| CR: Composite reliability, R2: Square of the correlation, AVE: Average variance extracted, statistical significance level is at 0.01 and diagonal figures mean | |

| Table 3: | Research hypotheses test results |

| |

| Coefficient refers to the Beta (β). t-stat is the t-value. 95% confidence level | |

Table 2 below shows the results of factor analysis affecting Biomass Power Environmental Impact. The data also shows the CR values are higher than 0.60, with all AEV values higher than 0.50 for all values and R2 values higher than 0.20, representing the reliability of the measurement. It found that data sets in the ![]() have higher values than all of the corresponding values in the ‘Cross Construct Correlation’ in the same column, representing discriminant validity of the measure in each construct and with a greater value than 0.50 of AVE as shown in Table 2. The samples were analyzed to answer the research hypotheses criteria in the three assumptions presented in Table 3.

have higher values than all of the corresponding values in the ‘Cross Construct Correlation’ in the same column, representing discriminant validity of the measure in each construct and with a greater value than 0.50 of AVE as shown in Table 2. The samples were analyzed to answer the research hypotheses criteria in the three assumptions presented in Table 3.

Furthermore, the structural analysis model framework was used to research the t-test coefficients and their relationship of each path of the t-test hypothesis with significance greater than 1.96. This explains the results obtained from analysis as shown in Table 1 and 2 as well as the test results presented in Table 3 below.

RESULTS

Property includes land and buildings and the land is classified as a limited natural resource. Today's technology is capable of augmenting this resource to some degree such as building tall towers or filling in sea for expansion and development, but overall urban areas are limited and property development has to be carefully considered. The Thai government should create incentives and encourage investment from both Thais and foreigners whose investment aims are residential, farming or industry and manufacturing.

Therefore, consumers need to consider the economy and investment situation to see if investments make economic sense to invest or not. Investment costs, such as interest rates, can result in whether a return on investment is attractive to investors or not. There are also other factors that affect investment decisions by government policies, such as the promotions, investment finance measures, tax incentives and legal and regulatory measures.

There are also community related social and environmental factors such as community relations, the availability of utilities, international linkage systems, sanitation systems, etc. So you can see that all these factors are involved in investments which will affect investment patterns, both direct investment and indirect investment, which is linked to behavior and the type of land holdings.

CONCLUSION

Thailand is on the precipice of change. The country has experienced amazing growth and prosperity to it economy, mainly due to foreign direct investment in various forms across many sectors of its economy. Government policy has also had a huge influence on this investment as can be seen from the policies and statistics from Thailand’s Board of Investment (BoI). Pattaya and Bangkok have seen their property markets explode with premium commercial property in Bangkok soaring to US$50,000 for 4 square meters. This however is dependent on factors that appear to be changing rapidly has this study is being finished.

Sadly, Thailand is undergoing another convulsion of change. With this change, hopefully for the better, is uncertainty and chaos. What the study does show conclusively is that the economy and investment have a positive and direct influence on foreigner’s desire to hold real estate in the kingdom. It also has been established that government policy has a direct and positive effect on the economy and investment as well as real estate holdings by foreigners. This assumes however that governmental policy is transparent and favorable for the foreign investor.

Thailand has entered another chapter of its long history with the coup of May 2014. Where it exits and under what circumstances is anyone’s guess and how it affects foreign investor sentiment is beyond the scope of this research. That as they say, is for another day.

REFERENCES

- Adelaja, A.O., Y.G. Hailu, A.T. Tekle and S. Seedang, 2010. Evidence of land hoarding behavior in US agriculture. Agric. Finance Rev., 70: 377-398.

CrossRef - Keng, C.H., 2009. The three pillars of the ASEAN community: Commitment to the human rights process. Proceedings of the 5th Roundtable Discussion on Human Rights in ASEAN-Towards an ASEAN Human Rights System: Role of Institutions and Related Activities, December 15-16, 2009, Bangkok.

Direct Link - Camilleri, D., 2011. A long-term analysis of housing affordability in Malta. Int. J. Housing Markets Anal., 4: 31-57.

CrossRefDirect Link - Henseler, J., C.M. Ringle and R.R. Sinkovics, 2009. The Used of Partial Least Squares Path Modeling in International Marketing. In: New Challenges to International Marketing (Advances in International Marketing, Volume 20), Sinkovics, R.R. and P.N. Ghauri (Eds.). Emerald Group Publishing Limited, Bingley, UK., ISBN-13: 9781848554689, pp: 277-319.

Direct Link - Mohd, I., F. Ahmad and W.N.W.A. Aziz, 2009. Exploiting town planning factors in land development: Case study of urban housing in Kuala Lumpur, Malaysia. J. Facilities Manage., 7: 307-318.

CrossRefDirect Link - Cohen, L.M., 2010. Physical assets in the M and A mix: A strategic option. J. Bus. Strategy, 31: 28-36.

CrossRefDirect Link - Lopez, R.A., A.O. Adelaja and M.S. Andrews, 1988. The effects of suburbanization on agriculture. Am. J. Agric. Econ., 70: 346-358.

CrossRefDirect Link - Dowden, M. and E. Humphreys, 2013. Landlord and tenant update-hard times, strict compliance. J. Property Invest. Finance, 31: 101-105.

CrossRefDirect Link - Omran, M.M. and J. Pointon, 2009. Capital structure and firm characteristics: An empirical analysis from Egypt. Rev. Accounting Finance, 8: 454-474.

CrossRefDirect Link - Wingwon, B. and M. Piriyakul, 2010. Determinants of perceived performance perceived CSR, perceived product and service quality, customer citizenship behavior of modern trade in Northern region Thailand. Proceedings of the International Conference on Toward Enhancement of Economic, Social, Technological and Environmental Development for Welfare Implications in the Greater Mekong Sub-region and Asia-Pacific, July 31-August 5, 2010, Yogyakarta, Indonesia, pp: 1-18.

Direct Link - Chan, N. and F.Y. Chen, 2011. A comparison of property taxes and fees in Sydney and Taipei. Property Manage., 29: 146-159.

CrossRef - Tan, R.M.K., 2004. Restrictions on the foreign ownership of property: Indonesia and Singapore compared. J. Property Invest. Finance, 22: 101-111.

CrossRefDirect Link - Rovinelli, R.J. and R.K. Hambleton, 1977. On the use of content specialists in the assessment of criterion-referenced test item validity. Dutch J. Educ. Res., 2: 49-60.

Direct Link - Roubi, S. and A. Ghazaly, 2007. Pricing inter-neighbourhood variation: A case study on the rental apartment market in Greater Cairo. Property Manage., 25: 68-79.

CrossRefDirect Link