Salami Dada Kareem

Faculty of Economics and Administration, University of Malaya, Kuala-Lumpur, Malaysia

Fatimah Kari

Faculty of Economics and Administration, University of Malaya, Kuala-Lumpur, Malaysia

Gazi Mahabubul Alam

Academic Performance Enhancement Unit, Office of the Vice Chancellor, University of Malaya, Kuala-Lumpur, Malaysia

G.O. Makua Chukwu

Faculty of Social Sciences, Lagos State University Ojo, Lagos, Nigeria

M. Oke David

Faculty of Social Sciences, Lagos State University Ojo, Lagos, Nigeria

The International Journal of Applied Economics and Finance

Year: 2012 | Volume: 6 | Issue: 4 | Page No.: 127-135

ABSTRACT

This study investigates the impacts of Foreign Direct Investment in oil sector in Nigeria and its attendant impact on economic growth. The co-integration analysis was employed for the study. The results showed that Foreign Direct Investment at current year is negatively associated with GDP possibly due to the fact that such investment needed to be allowed some time lag to translate to any significant impact. The impact of domestic capital formation is relatively small compared with the impact of Foreign Direct Investment in the oil sector. This is a further evidence of the dominant role of foreign investors in the oil sector of the country. Therefore, addressing problems related to security, corruption, inadequate infrastructure and inconsistent regulations remains the key elements of Nigeria’s future challenge of attracting more efficiency-seeking Foreign Direct Investment that can promote her economic growth. The Foreign direct investment is significant to the expectations of improvement of Nigeria’s economy, as it is a way of growing the capital existing for savings. And the economic growth required lessens deficiency and elevate standards of living.

PDF Abstract XML References Citation

How to cite this article

Salami Dada Kareem, Fatimah Kari, Gazi Mahabubul Alam, G.O. Makua Chukwu and M. Oke David, 2012. Foreign Direct Investment into Oil Sector and Economic Growth in Nigeria. The International Journal of Applied Economics and Finance, 6: 127-135.

DOI: 10.3923/ijaef.2012.127.135

URL: https://scialert.net/abstract/?doi=ijaef.2012.127.135

DOI: 10.3923/ijaef.2012.127.135

URL: https://scialert.net/abstract/?doi=ijaef.2012.127.135

INTRODUCTION

Foreign Direct Investment (FDI) inflows to Nigeria dropped considerably between 2009 and 2010 by $3.7bn from $6bn in 2009 to $2.3bn in 2010 (UNCTAD, 1999, 2006, 2007). This immense fall of 60.4 percent shows the need for Nigerian government to begin to rigorously and courageously address the challenges to foreign investment and other business interests in the country. The UNCTAD report noted that investment inflow into Nigeria and the rest of Africa increased substantially in 2008 but declined significantly in 2009. In spite of economic reforms by the government, no appreciable improvement was made. Insecurity in the land is a likely primary factor responsible for the sharp decline. This is a true reflection of Nigeria’s economic, social, legal and cultural environment which raises several questions and anxiety from prospective foreign investors.

The “Boko Haram” insurgence since 2010 in Nigeria is receiving attention from the governments. The tranquility presently enjoyed in the Niger Delta region of Nigeria brought about by the amnesty and post-amnesty programs is worthy of note. This has improved the macroeconomic environments in the oil sector. The ongoing reforms in the financial sector as well as government commitment to tackle the challenge of inadequate power supply are other sources of encouragement. There seemed to be some renewed confidence in investing in the country.

From 1970-1990, Nigeria accounted for 30% of FDI inflow to Africa; this was largely as a result of its oil attractiveness UNCTAD, 1999. However, in 2007 in spite of the oil boom, Nigeria accounted for only about 16% of total FDI inflow to Africa. Its most important role in terms of attracting FDI started grinding down due to the surge of FDI to other oil-rich countries, such as Angola and Sudan. Another factor is the improved FDI performance of other large African countries such as Egypt and South Africa which are successful in attracting FDI in various sectors of their economies (Ibi-Ajayi, 2006).

In many developing countries, privatization has been a very important source of FDI over the last two decades. Nigeria has implemented two rounds of privatization since 1980s (United Nation, 2009). The first part of Structural Adjustment Programmed (SAP) was in 1986-1993 and the second one was introduced in 1999. Africa and Nigeria in particular joined the rest of the world in search of FDI as evidenced by the formation of the New Partnership for Africa’s Development (NEPAD) which has the desirability of increasing foreign investment to Africa as a major component (Ibi-Ajayi, 2006).

The UNCTAD World Investment Report in 2007 shows that FDI inflow to West Africa was dominated by inflow to Nigeria which received 70% of the sub-regional total inflow and 11% of Africa’s total inflow. Out of this, Nigeria’s oil sector alone receives 90%. Studies have attempted examining the determinants structure and potentials of foreign direct investment in Nigeria (Odozi, 1995; Anyanwu, 1998). Others have focused on the magnitude of direction and prospects of foreign direct investment (Jerome and Ogunkola, 2004; Ayanwale and Bamire, 2001). However, evidence on impact of foreign direct investment on the oil sector and the economic growth in Nigeria remains scanty. Therefore, the objective of this study is to examine the economic growth evidence of FDI in the oil sector. However, the paper will establish the nexus between FDI into oil and Nigeria’s economic growth performances.

LITERATURE REVIEW

Economic theories and empirical studies support the notion that foreign direct investment is conducted in anticipation of future profit. It is generally assumed that investment flows from regions of low anticipated profit to those of high anticipated ones, after allowing for risk. Although, expected profits may ultimately explain the process of foreign direct investment, corporate management may emphasize a variety of other factors when considering investment motive. These factors include market-demand conditions, trade restriction, investment regulations, labour cost and transportation cost (Kim and Seo, 2003).

The neoclassical economists argue that FDI influences economic growth by increasing the amount of capital per persons. Bengos and Sanchez-Robles (2003) assert that even though FDI is positively correlated with economic growth, host countries require minimum human capital, economic stability and liberalized markets in order to benefit from long-term FDI inflows. Capital from external country can be very helpful in speeding up the rate of economic growth and can act as a catalytic agent in making it possible to exploit natural resources predominantly in a developing country. Foreign investment inflow can, at best be complementary to domestic savings. In developing economies, literatures have shown that foreign investment unaccompanied by domestic investment cannot create any stable basis for higher standard of living in the future.

Alfaro (2003) noted that FDI impacts on growth differ across sectors. The benefit depends on the spread out potential of the industry. Further studies also draw consideration to the fact that the benefits of FDI on growth cannot be generalized across different countries or sectors. Each has certain specific conditions that characterized market which could improve or hamper these benefits on the host country’s economic growth. However, despite these conflicting views on the relationship between FDI and growth, it is still highly recommended that emerging markets should actively pursue FDI (Nwankwo, 2006).

The central point on FDI and economic growth can be generally classified into two. First, FDI is well thought-out to have direct impact on trade through which the growth progression is assured (Markussen and Vernables, 1998). Second, FDI supplements domestic capital thereby stimulating the productivity of domestic investments (Borensztein et al., 1998; Driffield, 2001). These two arguments are in conformity with endogenous growth theories (Romer, 1990) and cross country models on industrialization (Chenery et al., 1986) in which both the quantity and quality of factors of production as well as the alteration of the production progression are components in developing a competitive advantage. FDI has empirically been found to stimulate economic growth by an integer of researchers (Borensztein et al., 1998; Glass and Saggi, 1998; Vu, 2008).

De Mello (1997) identified two channels through which FDI may be growth attractive: FDI might promote knowledge transfers; both in terms of labor training and skill attainment and better management. FDI can also promote the implementation of new technology in the production process through capital spillovers.

Greenaway et al. (2007) noted that developing countries with progressively more liberal trade policies are the ones with upward ratios of trade and inward investment to national income and with advanced growth rates. Fosu and Magnus (2006) examine the long-run impact of foreign direct investment and trade on economic growth in Ghana between 1970 and 2002. Using an augmented aggregate production function growth model and by applying the bounds testing approach to co-integration, they found long-run relationship between growth and its determinants in the aggregate production function model. The consequences of their work pointed toward negative impact of FDI on growth which is a divergence from most past studies. Trade however, was found to have considerable positive impact on growth.

THEORETICAL FRAMEWORK AND RESEARCH METHODOLOGY

Given that FDI requires time lag for its effect to become evidence, a dynamic regression analyses as well as co-integration approach was used in this paper. The neoclassical Cobb-Douglass production function provides the theoretical framework for this study. This production function which has been widely applied in the analysis of foreign direct investment and trade impact on growth, assumes unconventional inputs such as foreign direct investment and trade openness along with the conventional inputs of labor and capital in the model.

Our approach follows that of Fosu and Magnus (2006). The aggregate production function is specified as follows:

| (1) |

where, GDP is the aggregate production of the economy at time t; At, Kt and Lt denote the Total Factor Productivity (TFP), capital stock and labour at time t, respectively. Subsequent to the Bhagwati’s hypothesis, it is implicit that foreign direct investment, trade openness and other factors which are exogenously determined, establish the behavior of TFP (Bhagwati, 1978; Edwards, 1998). Therefore, the TFP is specified as:

| (2) |

Equation 2 can be expressed as:

| (3) |

Substituting Eq. 3 into 1 give:

| (4) |

To estimate Eq. 4, we take the natural logs of the right side of the equation. This is shown in Eq. 5:

| (5) |

Ct represents a constant parameter, μ denotes the error term and gdpt, kt, It , fdit and trt , remain as earlier defined. The terms α, β, ø and δ are coefficients of the parameters of kt, It, FDIt and trt, respectively. All coefficients are expected to be positive.

Our first step was to examine the characteristics of the data in order to determine whether or otherwise the variables have unit roots that is, whether they are stationary or not. In this paper, stationarity tests were conducted using Augmented Dickey-Fuller (ADF) and Phillips-Perron (PP) unit root tests at 5% level of significance. The variables that were found not to be stationary at its level (i.e., zero integration) were difference till they achieved stationarity. Thus, all the variables were used at their levels of stationarity. Of course, this enhances the predictive power of the regression results.

To estimate the relationships among the variables of interest, this study employs the Distributed Lag (DL) model approach stipulated by Pesaran et al. (2001). However, following Occam’s razor principle of parsimony the DL regression model would be kept as simple as possible. Occam’s razor principle states that if we can explain the behavior of Y “substantially” with two or three explanatory variables and if our theory is not strong enough to suggest what other variables might be included, why introducing more variables (Gujarati, 1995, 2004).

The Nigerian annual time series data from 1980-2007 on these variables: output (GDP); Foreign Direct Investment in the oil sector (FDI); Trade Openness (TR); Labor Stock (L) measured in terms of labor force and capital stock (K) measured by gross capital formation were sourced from Central Bank of Nigeria Statistical Bulletin, National Bureau of Statistics and World Development Indicator (WDI). The variables are expressed in their per capita values and stated in real terms.

PRESENTATION AND EVALUATION OF RESULTS

From the results of the augmented Dickey-Fuller (ADF) and Phillips-Perron (PP) unit root tests at 5% level of significance, none of the variables achieved stationary at level apart from TR using Phillips-Perron unit root test. Only Foreign direct investment in oil (FDI) achieved stationary after first difference. Using both methods, Gross Domestic Product (GDP) and Labor (L) achieved stationary after the second difference.

| Table 1: | Johansen co-intgration test |

| |

| *(**) dnotes rejection of the hypothesis at 5% (1%) significance level, L.R. test indicates 2 co-integrating equation (s) level, Series: D(GDP, 2) D (Log (L), 2), Large interval: 1-1 | |

| Table 2: | Dynamic regression |

| |

| Dependent Variable: D(GDP,2), Method: Least Squares, Date: 05/12/11 Time: 17:28, Sample(adjusted): 1984 2007, Included observations: 24 after adjusting endpoints | |

| Table 3: | Economic expected signs |

| |

Using Augmented Dickey Fuller (ADF) method, Capital (K) became stationary after 4 times difference but became stationary after the first difference using Phillips-Perron (PP) method. Therefore, to avoid losing high degree of freedom, the regression analyses are based on the use of Phillips-Perron test. We suspected co-integration between GDP and labor since they both achieved integrated at the same order. Thus, co-integration test was conducted as shown in Table 1 below.

The above Johansen Co-integration test shows evidence of co-integration or long-run relationship or equilibrium between GDP and labor since the values of Likelihood ratio of the test is greater than the critical value at 5% level of significance. To ensure that this long-run relationship does not bias the estimate of labor on GDP, error correction mechanism was generated and introduced in the model.

Table 2 below presents the economic test of the regression result.

Economic test: As shown above, all the independent variables in the model conform to the expected positive sign except the first differenced FDI. The possible reason for the variant is explained below in the ‘discussion of main results.’

| Table 4: | Correlation matrix |

| |

| |

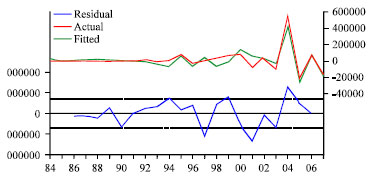

| Fig. 1: | The R2 fitted trend |

Testing for autocorrelation and multicollinearity problems

Autocorrelation test: One of the major assumptions of Least Squares is that there is no correlation between the disturbances. Thus, the null hypothesis states that there is evidence of autocorrelation. That is:

Ho: Cov(μi, μj /xi, xj) ≠ 0

where, xi and xj are any two independent variables.

The presence or absence of autocorrelation in the model was tested using Durbin-Waston (Dw) statistic test. According to Gujarati (1995), given N = No. of observations and K1 = No. of explanatory variable: If Dw < dl: there is evidence of positive first-order serial correlation. If Dw>du: there is no evidence of positive first-order serial correlation. But if dl<Dw<du: there is inconclusive evidence regarding the presence or absence of positive first-order serial correlation. where, dl and du are lower and upper limits of Durbin-Watson, respectively. From Table 3, Dw = 2.023848, N = 24, K1 = 6; Thus, dl = 0.837, du = 2.035. Thus, since the Dw (2.023848) of the model falls between dL (0.837) and du (2.035), we conclude that there is little or no evidence of positive first-order serial correlation. This implies that the estimates and inferences that will be drawn are reliable.

Multicollinearity test: The result in Table 4 shows that there is no serious pair-wise correlation between any two different regressors in the model since none of the correlation co-efficient is in excess of 0.8. This implies that all the estimates show an independent and unbiased impact on the dependent variable.

Diagnostic statistical test: The result shows that the co-efficient of multiple determinations (R2) of the model is R2 = 0.801818 with adjusted R2 as 0.73171.

| Table 5: | t-statistic test |

| |

This implies that approximately 80% of the variation in the GDP is explained by the independent variables in the model. This is shown Fig. 1 as the fitted trend is seen running almost superimposed on the actual trend of GDP:

Since, the Fcal (11.46327)>Ftab (2.66), we reject our Ho and conclude that the estimates of the parameters are simultaneously significant. This is further confirmed by the F-probability (0.000036) which is significantly low.

Evaluation of hypothesis: The statistical significance of each coefficient of the dynamic regression model is summarized in Table 5.

DISCUSSION OF MAIN RESULTS

From Table 5, both first differenced FDI and first differenced capital (K) were found to have significant negative and positive impact, respectively, on economic growth (GDP); while labor (L) and trade openness (TR) are not statistically significance. However, third lag of FDI shows positive statistically significant impact on GDP. The implications of these findings are discussed in turn.

It is important to observe that FDI was used in its first difference and third lag. This was to ascertain the dynamic nature of FDI. Although, two of them are significant, the result shows that first differenced FDI is negatively associated with GDP. It could be because, such investment needed to be allowed some time lag to translate to any significant impact. Thus, considering investment in a short-run vis-à-vis returns may inform why the negative impact was observed. However, after the foreign investment into the oil sector is allowed three years lag time, it showed a positive significant impact on GDP. Specifically, the result shows that a unit increase in foreign direct investment into the oil sector at lag 3 will increase Nigeria’s GDP by approximately 16 units. The level of impact could be because the oil and gas sector of Nigeria is mainly managed by foreign investors.

Nigerian economy has high propensity of return on capital. This could be seen in the impact of domestic capital on GDP as captured in the result of the analysis. The result shows that capital has significant positive impact on GDP. A unit increase in domestic capital formation in Nigeria increases GDP by about 1.7 units. Well, this may be attributed to the joint venture of the Federal Government of Nigeria through the Nigerian National Petroleum Corporation (NNPC) and foreign investors in Nigerian oil sector (such as Shell, Exxon-mobile, Total, etc.). The impact of domestic capital formation is relatively small compared with the impact of FDI in the oil sector. This is a further evidence of the dominant role of foreign investors in the oil sector of the country.

As stated earlier, at lag 2, labor was found to be positively related to GDP growth rate. However, it shows insignificant impact on the economy. This may be because of the low level of technological development in the economy which rather seems to be labor intensive and the fact that not many Nigerians work as experts in the major sector that drives the economy-oil and gas sector. Therefore, improving the quality of labor in Nigeria is highly recommendable.

Nigerian economy depends highly on foreign trade. This is made obvious in the result of the analysis which shows that trade openness at lag 1 has positive relationship with GDP. However, the result shows that the aggregate impact of openness has not affected the economy significantly. This could be because the economy depends so much on imported goods and services which had adversely affected its foreign revenues.

CONCLUDING REMARKS

The deteriorating rule of law and political instability, as well as institutional challenges in Nigeria have discouraged FDI and trade flows outside the oil sector. Addressing problems related to corruption, inadequate infrastructure and inconsistent regulations remains the key element of the country’s future prospects of attracting more efficiency-seeking FDI. There is necessity for a relevant policy towards FDI that involves the improvement of national laws that are in agreement with international practices.

National income should be enhanced by diversifying the export base of the economy from oil to non-oil since the country’s trade opening is not significantly impacting the economy at present. Besides, efforts should be made to refine all the derivatives of oil at home while manufacturing activities should be promoted since primary product exports suffer secular deterioration in term of trade. The rapid growth experience of the newly industrializing countries has shown the importance of successful manufacturing activities at home on economic growth and development.

Portfolio equity flows to developing countries are very likely to be exceedingly responsive to a country’s openness, mainly the governmental rules relating to the repatriation of assets earnings. The right to send back dividends and assets may be the most vital factor in attracting considerable foreign flow of equity.

Since, rent seeking and corruption are manifestations of inefficient and ineffective public institutions and absence of good governance, therefore, government should provide good leadership, proper accountability and transparency. Good governance should provide the lead in the development process; this implies that Nigeria should embrace governance led development strategy. Priority should be given to human capital development which is an important requirement for growth and development.

REFERENCES

- Bengos, M. and B. Sanchez-Robles, 2003. Foreign direct investment, economic freedom and growth: New evidence from Latin America. Eur. J. Political Econ., 19: 529-545.

CrossRef - Borensztein, E., J. de Gregorio and J.W. Lee, 1998. How does foreign direct investment affect economic growth? J. Int. Econ., 45: 115-135.

CrossRefDirect Link - Kim, D.D.K. and J.S. Seo, 2003. Does FDI inflow crowd out domestic investment in Korea? J. Econ. Stud., 30: 605-622.

CrossRef - Greenaway, D., D. Sapsford and S. Pfaffenzeller, 2007. Foreign direct investment, economic performance and trade liberalisation. World Econ., 30: 197-210.

CrossRef - De Mello, Jr.L.R., 1997. Foreign direct investment in developing countries and growth: A selective survey. J. Dev. Stud., 34: 1-34.

CrossRefDirect Link - Edwards, S., 1998. Openness, productivity and growth: What do we really know? Econ. J., 108: 383-398.

CrossRef - Fosu, O.A.E. and F.J. Magnus, 2006. Bounds testing approach to cointegration an examination of foreign direct investment, trade and growth relationships. Am. J. Applied Sci., 3: 2079-2085.

Direct Link - Glass, A.J. and K. Saggi, 1998. FDI policies under shared markets. J. Int. Econ., 49: 309-332.

CrossRefDirect Link - Markussen, J.R. and A.J. Vernable, 1998. Multinational firms and the new trade theory. J. Int. Econ., 46: 183-203.

CrossRefDirect Link - Romer, P.M., 1990. Endogenous technological change. J. Political Econ., 98: S71-S102.

CrossRefDirect Link - Vu, T.B., 2008. Foreign direct investment and endogenous growth in Vietman. Applied Econ., 40: 1165-1173.

CrossRefDirect Link

Evans Abuchi Reply

very useful