Arindam Banerjee

Indian Institute of Management, Vastrapur, Ahmedabad-380015, India

Dheeraj Awasthy

Senior Vice President, HSBC, Bangalore, India

The International Journal of Applied Economics and Finance

Year: 2012 | Volume: 6 | Issue: 1 | Page No.: 1-16

ABSTRACT

This study highlights the role of knowledge management in the long run, towards building efficient debt collection mechanism. It points out the need to invest in appropriate knowledge management solutions for the firms operating in developing markets, especially the ones in the early stages of the product life cycle, in order to build competitive advantages through efficiencies in internal operations in the long run. The study describes a methodology using an illustrative case study of a successful application of knowledge creation and data mining solution for efficient debt collection in a retail bank in the US. It further extends the learning from the case and highlights the challenges and opportunities of developing such systems in nascent markets which have less evolved credit handling practices.

PDF Abstract XML References Citation

Received: August 02, 2011;

Accepted: November 21, 2011;

Published: January 06, 2012

How to cite this article

Arindam Banerjee and Dheeraj Awasthy, 2012. A Customer Knowledge-based Analytic Approach to Enhance the Efficiency of Debt Collections. The International Journal of Applied Economics and Finance, 6: 1-16.

DOI: 10.3923/ijaef.2012.1.16

URL: https://scialert.net/abstract/?doi=ijaef.2012.1.16

DOI: 10.3923/ijaef.2012.1.16

URL: https://scialert.net/abstract/?doi=ijaef.2012.1.16

INTRODUCTION

Consumer finance companies across the world are putting a lot of emphasis on reorganising their back end collections operations. Debt collection has emerged as one of the most critical operation for these companies. In the United States, portfolio deterioration is noticable with consumer loan portfolios as delinquencies in the 4th quarter of 2008 were up to 3.22% (2.65% for the same period in 2007 and 2.90% in the 3rd quarter of 2008) with the most significant increases in mortgages and credit cards (AFSA, 2009a). Another report (AFSA, 2009b), states that average bankcard borrower debt (defined as the aggregate balance on all bank-issued credit cards for an individual bankcard borrower) inched upward nationally 0.82% to $5,776 from the previous quarter's $5,729 and 4.09% compared to the first quarter of 2008 ($5,548). Year over year, bankcard delinquencies increased 11% from 1.19 to 1.32%.

Similar trends are also reported from the United Kingdom. According to an article appearing in a leading trade publication about a year ago there has been rapid growth of consumer debt in the United Kingdom (£34 billion in the year 2000 with an average debt of £20,000 per capita) with loan-to-income ratios in the home loan sector increasing to 2.4. This coupled with a slowdown in the British economy portends higher rates of delinquencies for financial services firms to cope with. These trends indicate high pressure on the credit providers to prune their clientele to prevent future charge-offs and to employ better collection procedures to reduce delinquency among current customers.

The scenario is going to be no different in the newer markets also which have less evolved borrowers with comparatively unsophisticated credit handling practices. These markets also require better management of bad loans by service providers. Some people feel that managing bad loans is not a problem in the newer markets because companies operating in these markets follow strict measures to ensure that the clientele is of the premium segment. But with increasing competition, even in these markets, many service providers may find it necessary to develop new products for the sub prime markets which will entail astute management of credit risk through effective collection measures. Increased competition in the premium segments may put pressure on the interest rates such that increased focus on the unsophisticated borrower may be imperative for long term profitability. Thus re-engineering debt collection procedures to improve operational efficiency may be the imperative of the future given the gloomy forecasts of the world economy and the unabated consumer-spending rate.

This study described a methodology that has bearing to developing such solutions in the nascent as well as in the evolved markets. The methodology first entails a knowledge creation mechanism that integrates with the other knowledge repositories of the organization such as customer data and past financial transaction data to create a comprehensive knowledge structure about the customer. This knowledge is then used to develop an efficient debt collection heuristic to assign delinquent customers to the most effective collection mechanism in order to optimise net debt collection (total amount of debt collected minus the operational expenditure of instituting the collection procedure). This is important because alternate collection mechanisms, such as arbitration or litigation or employment of specialist collection agencies involve significantly different fixed costs associated with employing the procedure. For instance, for every account sent to arbitration in the US, the credit card provider has to commit to a $130 arbitration fee irrespective of the outcome of the case. Hence, developing a mechanism based on the knowledge base of organization to assign various accounts to various collection mechanisms becomes important. The study discusses a method to categorize customers to various collection mechanisms based on their predicted responsiveness to the initiative and brings out the importance of investing into right type of knowledge management and data mining solutions.

The arbitration route to effective debt collection: The case of collections procedures at a large retail bank: Although, the project undertaken was proprietary in nature, what follows is a description of the general methodology used to design effective backend customer handling facilities at a large bank in eastern United States. The details and the financial implications of the project are disguised to protect the interests of the bank.

During recent crisis, the operations head at this bank realized the need for streamlining the collection activities for the bank’s credit card operations. The write-off (bad debts written off as losses) rate was close to 12%. With an annual outstanding balance close to $ 30 billion in its credit card business, this implied that the bank was accumulating a significant amount of losses annually. Prudent measures were needed to arrest this negative trend. One of the major considerations in selecting arbitration as the first initiative was the high fixed cost to the bank for each delinquent customer (Appendix 1 for details of collection mechanisms). For every customer sent to arbitration, the bank had to pay up an arbitration fee of $130, irrespective of outcome. Hence, it was essential to send only those delinquent customers against whom the bank has a reasonable case for arbitration and who have the ability to pay up the debt amount as well as the arbitration fee.

Arbitration procedures in consumer debt collections: Traditionally, credit providers have resorted to litigation procedures available under the law of the state to coax their delinquent customers to pay up their debts. When all other reasonable means of persuasion are exhausted, creditors resort to this extreme measure. Certain countries, such as the United States, provide customers of financial products an additional protection against a litigation suit by making it mandatory for the dispute to be handled by an arbitration forum (acts as a semi-formal dispute handling body) prior to its decisions being ratified by the court of law. The ruling of the arbitration forum is binding in most respects and usually it can be converted into a judgement based on a routine filing at the court of law.

In the United States, two major recognised arbitration forums operate in the domain of consumer credit disputes, the National Arbitration Forum (NAF) and the American Arbitration Forum (AAF). The procedure of Arbitration for payment settlement in consumer credit (Fig. 1) is normally initiated by sending a letter of intent by the service provider to the delinquent customer about its decision to resort to arbitration procedures to recover the amount due from the customer. A month’s notice is given to the customer to respond favourably to the notification and if he decides to accede to the credit provider’s demand for payment of the debt, the arbitration application is dropped.

In the event of a non-response or unfavorable response to the letter, the service provider has to follow up its intention by filing for arbitration against the delinquent customers and paying up the arbitration fees to the body that oversees the process (NAF or the AAF).

The procedure normally takes about four months for completion from the time the application is filed. Usually, the arbitration forum refers the case to one of its arbitrators on roll who would send a communication to the delinquent customer regarding the procedure and invite a response. If there is a dispute on the amount or there is a grievance that the customer voices, a formal hearing is fixed between the two parties (service provider and the delinquent customer) to state their cases in the presence of the arbitrator. The arbitrator provides a ruling which becomes binding on the warring parties. If the ruling is in favour of the customer, the service provider has to drop the case for recovering the delinquent amount. Otherwise, the customer is obliged to pay up the delinquent amount as well as the arbitration fees. If the customer does not have the ability to pay the entire amount, the service provider may get the settlement ratified in the court of law and have the customer’s fixed assets attached to the delinquent amount. In some cases, as required, the customer’s wages are proportionately reduced to repay the delinquent amount on an instalment basis.

| |

| Fig. 1: | The arbitration process |

There are some general implications that can be drawn from the description of the arbitration procedure. One, it is expensive for the bank to institute this procedure for all its delinquent customers (the fee is $130 per filing) and two, it is a fairly prolonged process and there is no guarantee that the debt will be returned immediately after a favourable ruling is received by the service provider. Hence, judicious choice of customers who may be assigned to this collection procedure is very necessary to be able to make this a profitable venture. The organization had no idea about the profile of customers who should be sent to the arbitration. Hence, a knowledge creation mechanism (a pilot project) was set up to capture the appropriate customer profile to be sent through arbitration.

Designing the knowledge creation mechanism: Designing the appropriate operation for arbitration involved the following:

| • | Setting up the arbitration process at an appropriate level for the pilot |

| • | Selecting a random sample of delinquent customers to be sent through the process |

| • | Tracking the response or lack of response from each customer on an ongoing basis |

Setting up the arbitration process: Since this procedure was adopted for the first time, careful planning was required to set up the arbitration procedure. A separate routing channel was created in operations to allow selected arbitration cases to an Arbitration Collections Cell. The cell handled, (1) the generation of the letter serving as a notice to delinquent customers about the bank’s intention to seek arbitration, (2) it handled the telephone calls from the customers that were served notice and (3) transferred the relevant papers to the arbitration forum at the end of the notice period. The cell also tracked if the customers made the payment of their debt anytime during the process. Since this was a pilot study of a limited scale, the size of the arbitration cell was modest. The plan was to scale up the operations once a decision on a full roll out was made.

Selection of customers for arbitration: A random sample of customers was chosen for assignment to the arbitration process. The randomisation was undertaken after rejecting from the system non-operational cases such as accounts with no proper addresses, multiple names, cases with disputes etc. The premise was that it would serve no purpose to send such cases, as it would simply increase operating costs without commensurate return. The pool of cases (other than the ones mentioned above) were subjected to a random sort and a sample of fifteen hundred cases was selected over a period of about a month to be sent through the arbitration process. Simultaneously, another set of approximately twenty two hundred cases was flagged as control cases. The cases in the latter set were sent to the usual collection cells, already in place prior to the pilot operation. The control group served as a benchmark for evaluating the performance (response) of the arbitration group. This type of design is well known as the Champion-Challenger methodology to evaluate marginal efficiency measures.

The sample of customers was chosen from a pool of recent cases of delinquency. The logic applied was that delinquent cases who were identified and administered the appropriate collection procedure early enough (1-2 months delinquent) would have a higher chance of paying up than cases that were critically delinquent (6-7 months delinquent).

Tracking responses from delinquent customers: All customers’ accounts, both in the arbitration and the control groups were continuously monitored for any response or receipt of payment. Since the bank had established processes to track and update accounts based on any new payment or response behaviour, tracking responses was not a problem. A reporting system was created to track the number of customers paying up or responding positively (e.g., calling up the bank to promise to pay) on a monthly basis. The first month-end report from the time cases were assigned to the experiment coincided with the end of the arbitration notice period. This notice period was meant to provide a chance to the customers to pay up their dues and avoid any further action by the bank. The response to the letter served as the surrogate measure for the effectiveness of the letter threatening arbitration procedures.

Integrating the new information (from pilot) with existing knowledge repositories: The challenging part of the pilot operation was the identification of sources of data on the individual accounts. Any information piece available on the customers in other knowledge repositories of the bank that described his/her demographics, psychographics, past transaction and payment behaviour was identified and extracted. In addition, relevant syndicated sources of information on the customer’s dealings with other financial service providers were also identified. Following section details the other repositories that were used to create an exhaustive knowledge structure of each customer which was later used for data mining purposes.

Bank’s customer application database: At the time of a new application for credit, card providers collect information about the potential customer in a standardised format. This includes details regarding the customer’s address, income, age, education levels and other routine demographic characteristics that are kept on record. The application database contains the electronic version of these data and is often the primary source of information regarding individual characteristics of a respondent that can be used as predictor variables for segmentation.

Files from syndicated agencies specialising in collation of customer transaction history across service providers, e.g., credit bureaux: Syndicated agencies, also referred to as credit bureaux in the United States, collate credit handling history of all customers from most service providers and develop standardised models that predict a customer’s credit behaviour in the future based on his/her history of handling credit. These models are robust since they are built using the transaction history of a particular customer from multiple service providers (provided the customer uses multiple credit options). Also, the models are able to represent a larger cross section of the market since they are built by pooling data from a larger database unlike the ones available with a single credit provider. The disadvantage of these models is that they are standardised and hence, not always appropriate for custom applications for a particular card company. Nevertheless, credit bureaux are an excellent source for syndicated transaction data of customers from multiple sources. Also, the standardised outputs from prediction models run by these agencies are used as input into the custom models built by individual card companies (these outputs are better known as credit scores).

Bank’s internal customer transaction database: The bank’s internal databases on the history of transaction between the bank and a particular customer provide a rich source of information regarding the behaviour of the customer. Information such as, annual charges to the card and interest accrual and delinquency history (number of times the customer has been delinquent in the recent past and severity of his delinquency) may be candidate predictor variables about his payment behaviour in the future and therefore may help determine the “right” collection method to be used.

Bank’s internal customer-wise collections history database: To complement the data available from the bank’s internal transaction database, individual customer’s history of interaction with the collections department was accessed. This database contained information on any previous records of delinquency and the collection department’s interaction with the customer while recovering the delinquent amount. More specifically, it recorded instances of the number of promises to pay made by the customer in a previous delinquency, if he/she kept his promise and how much of what he/she promised was actually honoured. The bank could track at least three years of data on the exact payment behaviour of a delinquent customer.

Demographic data on customers provided by third party providers: The individual characteristics data available in the applications database can be augmented with data available from third party sources (Donnelley Marketing Services, CLARITAS and Metro Mail are the major providers of demographic data in the United States). Apart from individual level information, these sources provide information at the neighbourhood level (based on the address of the customer). Important neighbourhood level information such as racial mix, economic parameters, income distribution, real estate value are available from this database.

For the success of the project, it was crucial to have access to historical information which was, a) available for a majority of the customers, b) reliable and c) relevant for developing a prediction model. The net result of this pilot was to be able to send the appropriate set of customers to arbitration. In order to do so, a significant outcome of this project was to build a prediction model using the customer data on demographics and past behaviour which would be able to select the right customers to be sent to arbitration. Hence, identifying information sources on individual customers that could potentially be used as predictor variables was very important. At the same time, it must be pointed out that the model building exercise was exploratory in nature. Unlike conventional statistical model development, this model building exercise was undertaken with little prior notion about what variables or characteristics of customers would determine their responsiveness to an arbitration threat. Hence, it was necessary to access as many variables associated with delinquent customers as we could possibly locate to develop a robust model. In this respect, the model development process resembled a typical data mining exercise. In this study across the bank, 150 unique variables were identified that described an individual’s characteristics and past behaviour and were found suitable to be used as potential predictor variables.

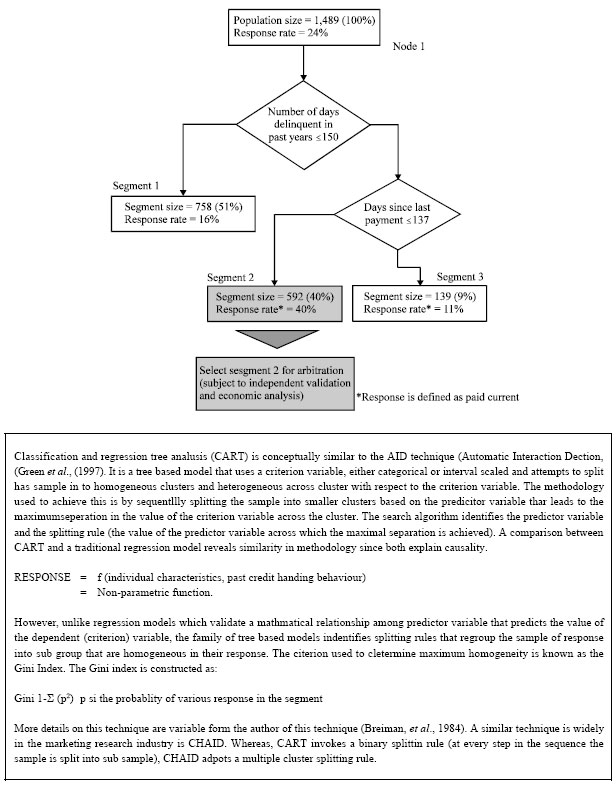

Developing an algorithm for routing cases through arbitration: The first attempt to develop a model based on the pilot result was made when a significant number of cases had been through the arbitration cell for at least a month. Across all the cases that had been sent to arbitration, the average positive response rate at the end of month 1 was about 24%. The response rate in the control sample was about 13%. Hence, it was concluded that the initial letter sent out to the customers served as a sufficient threat to increase the response rate significantly over the control group. However, the average response rate was not significantly higher to assign all customers to arbitration (given the cost involved). Hence, a non-parametric search procedure to identify segments of customers (based on the customer-related variables identified) was necessary. The objective was to uncover groups of customers who responded significantly more than the average response of the sample.

A Tree structured non-parametric data analysis was conducted on the data set consisting of the responses of the customers in the arbitration sample and their respective demographic and past behaviour data. This type of analysis is widely known as Classification Tree analysis. The analysis was performed on a sample of 1500 cases. This methodology employs a hierarchical rote search process by which it examines the separation between cases that respond and do not respond. The hierarchical combination of variables that splits the sample into groups that provide the maximum separation among the two response groups is chosen as the predictor model. The criterion used to decide on the best split at each level is the GINI index which measures the average incremental homogeneity within each sub node formed due to the binary split (for more details in Fig. 2). A set of about 150 candidate predictor variables was considered to evaluate the appropriate combination of customer variables that best separated the responders from the non-responders.

| |

| Fig. 2: | CART model for arbitration sample |

| Table 1: | Examples of customer characteristic variables used as candidate predictors in the tree model |

| |

Table 1 provides some details of the type of variables that were introduced in the prediction model. The model estimated is presented in Fig. 2.

Ideally, an unconstrained Classification Tree analysis will split the sample to the smallest sized terminal nodes determined by the number of possible combination of variables and their corresponding levels (Breiman et al., 1984). Also, a terminal node will have a size of at least one. For practical purposes, implementation of a viable strategy is a prime criterion for determining the terminal node size (segment size).

Constraints were sequentially imposed to obtain segment sizes (terminal node sizes) that were “viable” (considering both the level of homogeneity and size) and also meaningful in their description (based on the set of splitting criteria that determined the segment). The use of surrogates variables was considered, though not employed, wherein the splitting criterion was not found to provide a reasonable description of the segment. An iterative process was adopted to obtain convergence to a desirable segmentation output that reasonably satisfied all the issues raised above (Fig. 2), although no firm criteria were used to determine the selection of the output.

Interpretation of the model result: The model in Fig. 2 shows that, the original sample of respondents had a response rate of 24% (Node 1). In other words, 24% of the sample responded favourably to the letter sent out by the bank indicating their intention to initiate arbitration proceedings. The respondents either, called back and promised to pay up, or they sent in their payment for the amount due.

The algorithm identified the variable, “Number of Days Delinquent in the past year”, as the basis to split the sample in relatively more homogenous groups of responders versus non-responders. All cases which had exhibited less than 150 days of delinquency in the past year had a lower than average response rate of 16% (Segment 1). The cases that did not satisfy the above condition were further separated by the variable named ”Days Since Last Payment”. Cases that had made no payment in the past 137 days (the model classifies based on days since the variable is scaled on the number of days of no payment) were group as “Segment 3” and had a very low response rate of 11%.

The model identified “Segment 2” to be the most favourable in terms of response (40%). They were delinquent customers who had been in the delinquency pool for at least 150 days in the past year, but had paid up at least part of their debt periodically. This is indicated by the fact that they had made some payment to the bank in the past 3-4 months (137 days, as the model predicted).

The significance of this finding is that by calibrating the assignment rule for sending a debtor to arbitration, using his past delinquency history and payment patterns, may help yield a better “hit rate”. This is highly relevant for the bank since a high response to a letter stating intention to initiate arbitration reduces the liability associated with paying up the arbitration fees. Customers who have responded to the letter with a promise to pay the delinquent amount need not be sent to the arbitration council for subsequent hearing.

It may be prudent at this point to delve into the characteristics of the debtors who have responded favourably. Based on the characteristics of the segment identified by the model they can be described as customers who are more prone to remain delinquent as per the past year’s financial transactions. However, they appear to be relatively less serious cases of delinquency since they have made some form of payment in the recent past. One can reasonably conclude that they are not serious about meeting payment schedules and hence they remain in the delinquency pool for extended periods of time. It is fairly possible that these delinquent customers have the ability to pay up but are quite unwilling to pay on time since until now there were few options available to the bank to coerce them with censure. It must be pointed out that these are simply conjectures based on past financial transaction behaviour and in the absence of actual attitudinal data and appropriate demographic data (in spite of considerable efforts made to procure them), validating the above hypothesis is difficult.

Response rates in the control group: It is important to cross check whether the segment identified as responding to arbitration notice shows similar response in the control group. This is required to validate that the response generated can be directly attributed only to the threat of arbitration. However, if the segment exhibited a strong positive response regardless of the collection mechanism, it would be pointless to assign it to arbitration and unnecessarily expose the bank to an additional fixed expense of the filing fee.

Similar Classification tree analysis on the control group revealed Tree structure shown in Fig. 3. From an overall response rate of 13%, the model identified a small segment (size: 5% of original sample) which had a high response rate of 43%.

| |

| Fig. 3: | CART model within control sample |

Using the approach to describe the segments as explained earlier (see the section on Interpretation of Model Results), the description of the segment with the highest response rate (segment 1) revealed that they were debtors who had on an average an outstanding balance of less than 46% across all their credit instruments at any point in time. Also, they had not corresponded with the bank in the past 2 months. These delinquent customers may be classified as careless debtors who pay less attention to meeting up with their payment obligations on time. Yet they do not appear to be serious cases of delinquency wherein the debtor may not have the ability to pay up debts. This is inferred from the fact that they have a large percentage of their credit line remaining unutilised. The description of the responsive segment appeared seems somewhat similar to the segment that responded well to arbitration. To be absolutely sure that we would be sending only those customers who responded well to arbitration and not otherwise, we attempted to check the overlap between the responsive segments identified across both the arbitration and control samples to check if there is a significant overlap (this is required since the criteria determining the two segments are different across the two samples). The overlap was found to be insignificant. Hence, we concluded that the arbitration sample did reveal a unique segment that exhibited a high response rate, only when threatened with arbitration.

The average default response (response in the control group) of the arbitration segment was estimated by identifying those accounts in the control group that satisfy the criteria identified to send accounts to arbitration and calculating their average response. The default response rate was found to be 16%. Hence, the test pilot revealed an incremental response rate of 24% due to the initial letter dunning activity. This preliminary result was used to forecast the financial implication of arbitration, especially its role in reducing the final write-off percentage.

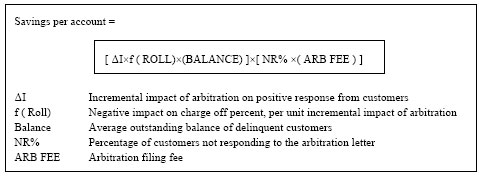

Financial implications of the arbitration proceedings: The net positive response of arbitration letter dunning activity was extrapolated in terms of its effect in reducing the write-off rate and hence its impact on reducing the losses to the bank (Fig. 4). The impact of a higher response rate is projected to estimate the net reduction in the flow of delinquent accounts towards charge-off (also known as roll-rate). A conservative estimate on reduction in charge-off and its impact on the additional savings led to an estimate of $217 per account. Since 40% of the accounts in the cardholder database (excluding the preliminary rejects) qualify to be assigned to arbitration, this amounted to savings of $40 million annually for the bank. The savings calculated took into account the number of new accounts that flowed into the delinquency pool each month. This is an estimate of saving based on the response rate. The actual saving is only observable through the reduction in the annual charge-off amount as depicted in the balance sheet. However, it is worth pointing out that the actual result could be due to a combination of reasons some of which may be beyond the control of the mechanisms that are being described in this study.

Follow up and validation: Based on the estimated positive impact, the management of the bank decided to increase the flow rate (number of accounts sent to arbitration each month), using the assignment rules identified. The initial samples sent using the new assignment rule served as validation for the estimated responses. The validation exercise lent credibility to the original estimates since the variance in the difference of the response rates between the arbitration segment and its corresponding response of the same profile in the control sample was of the order of ±8%. This was observed over samples that were run through the validation phase for over four months. With the passage of time, the original sample sent through arbitration revealed insignificant responses beyond the letter dunning stage. Most arbitration cases were approved in favour of the bank without a hearing; however, the immediate cash flow from them was negligible since payment was conditional on sale of assets in the customer’s possession. This usually resulted in delayed pay off cycle. Hence, it was concluded that the true potential of the arbitration process in securing immediate collections was mainly through the letter dunning process and that the prediction model needed to be refined to get a homogenous segment with higher response rate. This remains an opportunity for further research.

An area of concern regarding these pilot operations is the management of transition from the pilot phase to the actual roll out, especially when the results are optimistic. The scale of operations designed to man the process during the pilot phase does not match the enormous investments required to manage a full-scale roll out. The experience in this project has proven that transitioning from pilot to full scale operation requires considerable managerial prowess and requires significant attention.

| |

| Fig. 4: | Financial modelling framework for estimating savings to the bank through arbitration |

The scale up operation in this case led to an immediate reduction in efficiency of the operation. Shortage of staff to man the arbitration call centre and to file papers for the arbitration process rendered the collection operation inefficient. The implications are that organisations pursuing the option of redesigning their internal processes need to focus not only on the analysis and development of processes, but also on the seamless implementation of the processes. In this particular case, inefficient servicing of customer response was identified as the cause of subsequent reduction in arbitration response rather than inappropriate identification of cases for arbitration. A fall out of this underestimation in process design was a delay in proper commissioning of the operations by about three months. A substantial reassignment of call centre resources to handle arbitration responses and also the provision for a co-ordination cell to handle all pre and post arbitration paperwork were accomplished during this period. The delay in proper implementation of the arbitration process led to a loss of remittances over a two-month period while the process was still operational and costs were still being incurred.

Collection managers felt that the euphoria created due to the positive results from the pilot operation was considerably diminished due to the tardy handling of the transition to full-scale operation.

Creating a knowledge management solution: The learning’s from the case: The experience of creating a knowledge creation and utilizing mechanism to improve efficiency of collection operations at the bank emphasizes the need for the following:

| • | Creating right knowledge repositories that have customer level information in manageable format |

| • | Capturing right features in the databases that predict credit handling behaviour |

| • | Developing analytical resources to design and operate a knowledge creation operation and analyse data obtained from it to create the appropriate assignment rules |

| • | Developing managerial foresight and capability for timely design of appropriate internal processes to transform knowledge creation exercises into mainstream operations |

While each of these dimensions can become a sticky issue if adequate attention is not paid, many organisations may have limited potential to implement prediction model-based assignment rules as described above because of the paucity of right knowledge repositories. One of the major obstacles to using this approach is the significant investment costs and lead time required to build and maintain appropriate repositories that can be suitably mined for developing models that have been described earlier in this study. These issues need to be attended to while formulating the knowledge management driven strategy development initiatives, more so for the developing economies since they operate in the preliminary stages of the industry life cycle.

Appropriate investments in knowledge creation and knowledge storage for a significant period (our estimate would be a minimum of two years), will considerably enhance the probability of developing accurate analytical model based assignment rules for efficient collections process. The issue of investment in information resources for use in strategic initiatives is critical in a developing market because creditors will, sooner or later, face the problem of ensuring acceptable credit quality.

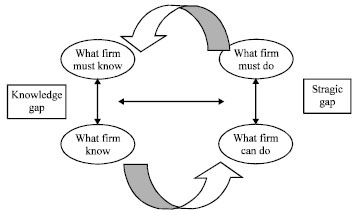

Meadows and Dibb (1998), also make a reference to such barriers in their article. Earlier in this study, it has been mentioned that the true nature of the customers who respond to the arbitration threat is not known and one can only speculate on their demographic and personality characteristics based on their past behaviour in the absence of better quality customer data. One plausible reason for this paucity of appropriate information could be traced to the original conception of knowledge management initiatives. Many databases developed in the banking sector are primarily “accounting” driven rather than “customer” or “market” driven. The knowledge management literature also suggests that organization should invest in developing knowledge repositories that capture external knowledge (e.g., competitive intelligence), structured internal knowledge (e.g., research reports, product-oriented marketing materials and techniques and methods) and informal internal knowledge (e.g., discussion databases full of know-how and lessons learned) (Davenport et al., 1997). The design and development of such repositories requires active participation by the main stream user groups of the organisations, namely the marketing and the operations functions. Historically, the development and maintenance of these knowledge repositories have been undertaken independently and sometimes divorced of the “true” needs of the line functions in the organisation. This may cause severe limitations on the usefulness of these repositories for business strategy development. The organization need to understand that knowledge is not just patents, or new discoveries but any information with added value and context. For example, Hooley and Saunders (1993) suggested that by adopting lifestyle based segmentation schemes, one may be able to predict customer behaviour and product requirements better. But they further mention that two out of three banks do not have necessary information to apply lifestyle-based segmentation.

Many developing markets may not have syndicated data collection agencies such as the credit bureaux like in the United States or other developed markets which collect and organise data across service providers and hence are able to provide a rich source of information about customers past credit behaviour. Thus an important challenge in these markets would be the availability of good reliable external sources of customer information. Some exploratory research by the authors among a few major credit card companies in one developing market revealed that a modest attempt has been made in this respect with service providers having come together to build a “negative file” which includes details of all customers who have had a history of serious delinquency with any one of the service providers. All card companies have access to this information which assists them in denying credit to the potentially most risky customers. Some other attempts at setting up a credit rating service have been recorded during our exploratory survey, although, the extent of the operation has yet to be ascertained.

CONCLUSION

Universally it is accepted that for survival in the long run in markets with diminishing opportunities for differentiation, implementation of cost-efficient backend operations is essential. In this regard, this study highlights an example of developing right knowledge repositories, prudent use of statistical modelling along with appropriate financial analysis to design an optimal debt collection procedure. The study shows the importance of identification of right type of data to be collected and then development of supporting processes and practices around it can give competitive advantage to corporate. While the specifics of collection mechanism may vary across environments, the premise for using a combination of experimentation and financial analysis to design the process has universal appeal.

Also, to be able to incorporate these best practices, some degree of information sharing in the industry is necessary through syndication of internal data across financial service providers. This last issue should be taken up as a tangible way forward for credit providers in developing markets to ensure better managerial systems in the future. With increasing knowledge intensive businesses the organizations in these markets will have to continuously generate, utilize and harness the knowledge both within and outside the organization to survive. The organizations in these markets should realize that knowledge is not something that is entirely stored within the internal systems but developing processes that help all the firms to share and utilize the common knowledge could lead to more benefits to all.

APPENDIX 1

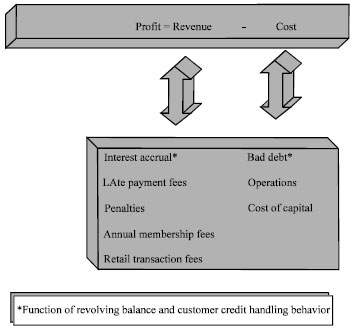

The business of consumer credit: The primary activity in consumer credit industry is to build and manage the credit balance outstanding. The revenue generation is through interest accrual which is directly related to total outstanding balance maintained by the company. However, the significant cost associated with managing consumer credit is due to non-payment of debts by customers leading to charge-off losses for the service provider. This loss is also proportional to the outstanding balance. Besides these major revenue and cost heads the service provider has to incur some minor operations costs of the card business. Some minor revenue heads such as penalties and fees levied by the service provider on customers who are not diligent about on time payment of their dues result in additional booked earnings for the service provider, although they are not critical enough to impact the viability of the business. The important issue for all credit providers is to develop a healthy customer base which will utilise the credit facility significantly, leading to healthy revenue generation and will not default on their payments to the company (Fig. 6).

In the late eighties, financial service providers in the United States invested in developing accurate customer acquisition models to develop a portfolio of clients that would be profitable based on the above rationale. These models were primarily based on statistical modelling techniques which predicted who would be a profitable customer. However, statistical models by their nature have a built-in inaccuracy due to the parsimonious design. Besides, the lack of appropriate input variables may be an additional cause of inaccurate prediction of a potentially profitable client. As a result of these factors, most customer acquisition models used by major financial services providers have had inherent flaws in their ability to predict who is likely to be a profitable customer (Chen and Chiou, 1999; Zhang et al., 1999).

Managing risk: A major dimension of operating a credit business is to minimise the risk associated with non-payment of outstanding balances.

| |

| Fig. 5: | Identifying the knowledge gap |

| |

| Fig. 6: | Operating model for a typical credit card company |

As mentioned above, inaccuracies in prediction models used for customer acquisition may lead to the burden of servicing clients who are habitually tardy about paying back their debts. Yet other customers may have started off with the good intention of using the credit facility extended to them by the service provider in a responsible manner but are beset with uncontrollable financial liabilities which upset their payment plans. Also, with increasing pressures of competition in the 1990s, service providers have been forced to look for revenue generation opportunities by knowingly soliciting relatively more risky segments (sub prime) of the consumers who are generally not sought after by many service providers (Watkins, 2000). For these reasons, debt collections have to be managed within acceptable norms to ensure that the charge-off rates do not spiral beyond control.

There are various debt collection initiatives that financial service providers across the world undertake to manage their inward cash flows. They range from periodic letter dunning, telephone calls and incentive (rewards) programmes to more coercive procedures such as instituting litigation/arbitration procedures or employing a specialist collection agency to retrieve the delinquent amount.

While service providers have an array of options to choose from, what is not so widely known is which of these techniques is most effective on what type of delinquent customer. To answer the above question, running a test pilot is necessary in order to assess the impact of each of these collection methods on a random sample of customers and then based on the sample result decide the best method of collection for each group, if they are identifiable (based on their individual characteristics and historical transaction data). An economic analysis which works out the net benefit of administering the specific collection practice on a set of customers less the cost of administration to determine the net payoff of collection can be used to identify customers who work out profitable for a particular collection method. For example, a rewards program that promises a release in credit line in lieu of payment of dues may seem to be effective measure to collect some outstanding balance from the most delinquent customers. However, it is quite likely that not all of these customers would use their open credit lines responsibly and the provider may in fact incur a loss on the new open credit line. Hence, for effective implementation of the rewards program, it should be offered to only those customers who are expected to assume greater responsibility in handling credit in the future. The focus of the problem therefore, is to develop the optimal routing algorithm to send each delinquent customer to the appropriate collection process in order to maximise the net inward cash flow in the future.

REFERENCES

- Breiman, L., J. Friedman, R.A. Olshen and C.J. Stone, 1984. Classification and Regression Trees. Wadsworth International Group, USA., ISBN-10: 0534980546, Pages: 368.

Direct Link - Chen, L.H. and T.W. Chiou, 1999. A fuzzy credit-rating approach for commercial loans: A Taiwan case. Omega, Int. J. Manage. Sci., 27: 407-419.

Direct Link - Meadows, M. and S. Dibb, 1998. Assessing the implementation of market segmentation in retail financial services. Int. J. Service Ind. Manage., 9: 266-285.

CrossRef - Watkins, J.P., 2000. Corporate power and the evolution of consumer credit. J. Econ. Issues, 34: 909-932.

Direct Link - Zhang, G., M.Y. Hu, B.E. Patuwo and D.C. Indro, 1999. Artificial neural networks in bankruptcy prediction: General framework and cross-validation analysis. Eur. J. Operat. Res., 116: 16-32.

CrossRefDirect Link