Alpana Vats

Economist, Andhra Bank, Saifabad, Hyderabad- 500004, India

The International Journal of Applied Economics and Finance

Year: 2011 | Volume: 5 | Issue: 4 | Page No.: 245-256

ABSTRACT

This research studies the long memory behavior of daily returns of Chinese Yuan (CNY), Indonesian Rupiah (IDR) and Taiwanese Dollar (TWD). Fractionally integrated models, ARFIMA and FIGARCH, were used to investigate the long memory property in returns and volatility, respectively. The results reveal that CNY and TWD exhibit long memory property in returns. All the three currencies exhibit long memory in volatility. The study further investigates the long memory dynamics in returns and volatility simultaneously using joint ARFIMA-FIGARCH model. The results indicate that there exists dual long memory in CNY and IDR which is better captured by ARFIMA-FIGARCH model under the assumption of skewed student-t distribution. The presence of long memory in returns of CNY and TWD implies that their behavior is predictable and hence, refutes the efficient market hypothesis. Likewise, the evidence of long memory in volatility reveals uncertainty or risk in the behavior of two exchange rates.

PDF Abstract XML References Citation

Received: November 01, 2011;

Accepted: December 20, 2011;

Published: February 22, 2012

How to cite this article

Alpana Vats, 2011. Long Memory in Returns and Volatility: Evidence from Foreign Exchange Market of Asian Countries. The International Journal of Applied Economics and Finance, 5: 245-256.

DOI: 10.3923/ijaef.2011.245.256

URL: https://scialert.net/abstract/?doi=ijaef.2011.245.256

DOI: 10.3923/ijaef.2011.245.256

URL: https://scialert.net/abstract/?doi=ijaef.2011.245.256

INTRODUCTION

The foreign exchange market of emerging economies of Asia has attracted attention all over the globe in recent years. The rapid economic growth in the Asian countries is accompanied by substantial increase in foreign exchange market turnover. The daily forex turnover of emerging countries of Asia has increased manifolds during the last few years. The foreign exchange markets of these countries are gradually deregulated and have become more matured. Today most of these countries have shifted to an arrangement commonly known as “managed float”. These countries allow the value of their currencies to adjust according to the market forces as long as the fluctuations in their value do not violate their other economic policy goal. As a result there has been increasing interest among researchers, investors and practitioners to understand the behavior of foreign exchange of these economies.

The conventional statistical techniques utilized by empirical research to study the behavior of exchange rates are based on the assumption of normality and random walk. These conventional techniques and tests fail to uncover the long range dependence in the exchange rate whose characteristics appear to conform more closely to observed financial returns. Hence, the present study tries to model long memory property of exchange rate using fractionally integrated techniques.

The long memory property is usually defined in relation to the autocorrelations of the process if the dependence between distant observations, although small, be significantly different from zero. This means that the effect of shocks on financial time series take a very long time to disappear. The presence of long memory in a series masks the true dependence structure (Mendes and Kolev, 2006) which implies a potential predictable component in the returns and volatility which in turn, may provide economic benefits available to speculators in foreign exchange markets. Furthermore, the derivative pricing models which are based on Brownian motion and martingale process become inappropriate in the presence of long range dependence.

Initially, research indicated considerable empirical evidence in support of long memory dynamics in exchange rates while more recent research has suggested that the empirical evidence is inconclusive, with results sensitive to the particular sample examined. For example, Booth et al. (1982), apply classical rescaled-range (R/S) analysis to daily exchange rates, find evidence of negative dependence during the fixed exchange rate period 1965-1971 and positive long-term dependence during the post-1974 flexible exchange rate period in three major exchange rates. Cheung (1993), employing the popular Geweke and Porter-Hudak (1983) estimator on five major exchange rates from 1974-1987, also finds evidence of long memory dynamics. Pan et al. (1996) provide additional evidence of long memory dynamics in this same sample, utilizing modified R/S and variance-ratio tests. Baillie and Bollerslev (1989, 1994) also find evidence of fractional integration in exchange rates. In contrast, Barkoulas et al. (2003) find little convincing evidence of long memory in 18 currency return series over the 1974-1995 period. They conclude that exchanges rate are best characterized as a martingale, rather than fractionally integrated. Some examples of recent studies analysing nominal exchange rate dynamics using fractional integration (looking at futures in particular) are those by Fang et al. (1994), Crato and Ray (2000) and Wang (2004). Volatility dynamics in foreign exchange rates (mainly the Deutsche mark vis-à-vis US dollar rate) have also been examined with the FIGARCH-model, introduced by Baillie et al. (1996) and subsequent papers using this approach are Andersen and Bollerslev (1997, 1998), Tse (1998-examining the Japanese Yen-US dollar rate), Baillie et al. (2000), Kihc (2004) and Morana and Beltratti (2004) analysing volatility.

Further, Ling and Li (1997) extended the ARFIMA process to an autoregressive fractionally integrated moving average with GARCH model (ARFIMA-GARCH) which has a fractionally integrated conditional mean with the GARCH to describe time-dependent heteroskedasticity. The idea of dual long memory process was first introduced by Teyssiere (1997) which show through Monte Carlo simulations that ignoring long memory in the conditional mean of a dual long memory process leads to significant biases in the estimation of the conditional volatility process. Consequently, in order to asses the robustness of the FIGARCH model the possibility of a fractional root in the conditional mean is introduced. They conclude that the ARFIMA-FIGARCH model capture more or less the dynamics of daily exchange rates, due to the fact that the fractional parameter in the mean equation was found to be quite low, confirming the presence of long memory only in the conditional volatility.

There is a voluminous literature on modeling long memory process in capital market. However, there is very few studies on long memory in foreign exchange market and even lesser related to long memory property in foreign exchange market of emerging economies. This study attempted to study the long memory property of three major currencies of emerging Asia namely Chinese Yuan Renminbi (CNY), Indonesian Rupiah (IDR) and New Taiwanese Dollar (TWD) against USD using fractionally integrated technique.

MATERIALS AND METHODS

Daily nominal exchange rates for Chinese Yuan Renminbi (CNY), Indonesian Rupiah (IDR) and New Taiwanese Dollar (TWD) against US Dollar have been examined. The time period covered for CNY is from 22 July 2005, date when China abandoned the fixed peg against dollar regime and shifted to more flexible regime, to 19 November 2010. The period covered for IDR and TWD is 1 July 1997 to 19 November 2010 and 24 August 1999 to 19 November 2010, respectively -the post deregulation period of these countries.

If a time series is I (0) then its ACF declines at a geometric rate. As a result, I (0) process have short memory since observations far apart in time are essentially independent. Conversely, if a time series is I (1) then its ACF declines at a linear rate and observations far apart in time are not independent. In between I (0) and I (1) processes are so-called fractionally integrated I (d) process where 0<d<1. The ACF for a fractionally integrated processes declines at a polynomial (hyperbolic) rate which implies that observations far apart in time may exhibit weak but non-zero correlation. This weak correlation between observations far apart is often referred to as long memory.

Generally, financial data series appear to have long memory, either in mean or in variance, which can be modelled using fractionally integrated models. Fractionally integrated processes have been applied both to ARMA models leading to ARFIMA models and to models of conditional volatility to lead to fractionally integrated GARCH and fractionally integrated stochastic volatility models. Long memory processes are reviewed in Robinson (1994) and Baillie et al. (1996). This study uses fractionally integrated autoregressive moving average (ARFIMA) models for the mean of the returns and fractionally integrated generalized autoregressive conditional heteroscedasticity (FIGARCH) models for the conditional volatility. The literature on long memory in returns and long memory in volatility evolved independently, as the phenomena seemed different and distinct. However, market shocks have a simultaneous impact on the conditional mean and conditional variance. Therefore, some recent empirical studies have focused on the relationship between the conditional mean and the conditional variance.

ARFIMA-FIGARCH model is suitable to estimate the long-term dependence in returns and volatility simultaneously in time series data. First component of the model, namely ARFIMA process, first appeared in finance literature in the studies of Granger and Joyeux (1980) and Hosking (1981). The model, known as Autoregressive Fractionally Integrated Moving Average (ARFIMA), allows for increased flexibility in modeling low-frequency dynamics. They proposed the following model:

An ARFIMA (p,ξ,q) model may be specified as:

| (1) |

where, {yt} is the process, φ (L) and θ (L) are AR and MA polynomials, respectively, in the lag operator L, p and q are the order of the AR and MA polynomials, respectively, ξ is the fractional difference parameter, μt is the white noise process. In Eq. 1 (1-L)ξ is defined as integration parameter:

| (2) |

where, ‘Γ’ is the gamma function.

ARFIMA process is nonstationary when ξ≥0.5. For 0<ξ<0.5, the process is said to exhibit long memory. For -0.5<ξ<0 is said to have short memory that is negative dependence between distant observations, called anti-persistence. The ARFIMA (p, ξ, q) model described above is used here to test for the presence of long memory in the returns process.

To check for presence of long-memory in volatility returns, the ARFIMA model given in Eq. 1 is extended to have ARFIMA representation in μt2. The extended model is known as FIGARCH (m, d, s) model due to Baillie et al. (1996). The FIGARCH (m, d, s) model may be specified as:

| (3) |

where:

|

where,

where, σ2t is the conditional variance of μτ.

The {v↓t} process is interpreted as the innovations for the conditional variance and has zero mean and serially uncorrelated. The roots of the polynomials φm (L) and [[1-πs] (L)] lie outside the unit circle.

The model given in Eq. 3 provides greater flexibility for modeling the conditional variance, as for d = 0, Eq. 3 is covariance stationary GARCH and d = 1, it yields the non-stationary GARCH. For 0<d<1, the model allows for intermediate range of persistence, giving rise to long term dynamics of volatility.

Preliminary analysis of the data: Descriptive statistics for daily nominal percentage returns series of CNY, IDR and TWD is summarized in Table 1. It indicates that none of the currency series show normality. Both the skewness and kurtosis statistics indicate that the return series have higher peak and fatter tail distribution than a normal distribution. Likewise, the Jarque-Bera test (J-B) statistics also reject the null hypothesis of normality in the distribution of the return series at 1% significance.

We also examine the null hypothesis of a white noise process for sample returns using the Box-Pierce test statistics of the returns Q (20) and squared returns Qs (20) . According to the calculated values of the Q (20) and Qs (20) statistics shown in Table 1, the null hypothesis of no serial correlation is significantly rejected. Thus, we can conclude that there is evidence of serial dependence in the level of return series for all the above mentioned currencies. These findings imply that there is non-normality and serial correlation in the foreign exchange returns of three currencies.

| Table 1: | Descriptive statistics |

| |

| Q (20) is the Box-Pierce test statistics for the return residuals for up to 20th order serial correlation. * and ** indicate rejection at 5 and 10% significance level, respectively | |

EMPIRICAL RESULTS

Before testing the long memory property in the three currencies namely, CNY, IDR and TWD they are subjected to three unit root tests, i.e., Augmented Dicky Fuller (ADF), Phillips-Peron (PP) and Kwiatkowski, Phillips, Schmidt and Shin (KPSS) tests. The null hypothesis for former two tests is presence of unit root i.e., non-stationarity, I (1) process, in series contrary to the third test for which the null hypothesis is I (0), implying stationarity in series. The results of unit root tests for all currencies returns series are presented in Table 2. In the case of the ADF and PP test, large negative values for all cases support the rejection of the null hypothesis of a unit root, I (1) process, at the 1% significance level while the statistics of the KPSS test indicate that all return series are not significant for rejecting the null hypothesis of stationarity, I (0) process. All the three unit root tests support stationarity in all three currencies. Thus, the return series are stationary and suitable for subsequent tests in this study.

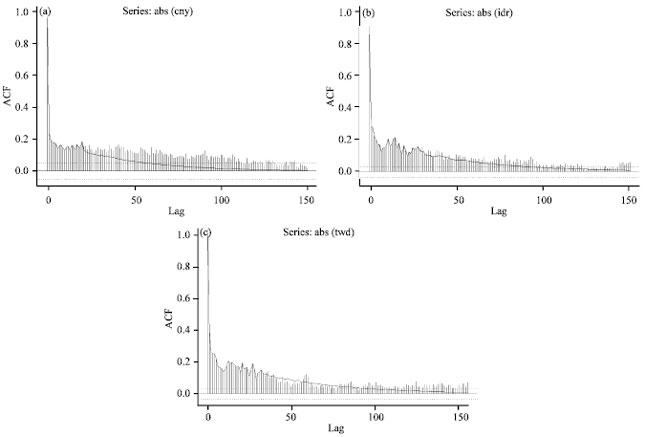

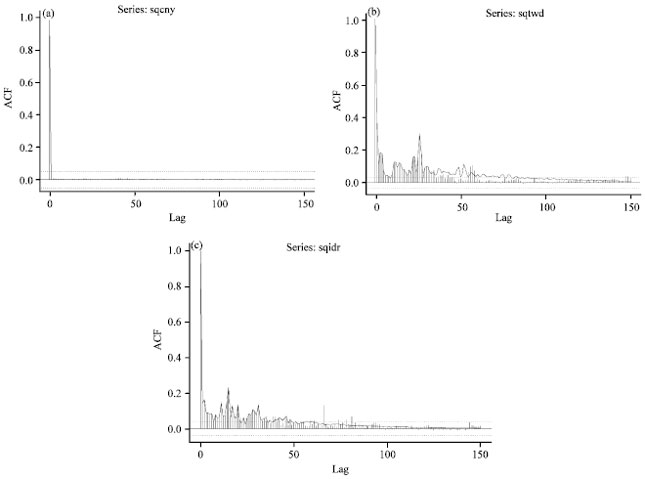

Graphical presentation: We begin by discussing the autocorrelation plots. As discussed earlier, the ACF for a fractionally integrated processes declines at a polynomial (hyperbolic) rate which implies that observations far apart in time may exhibit weak but non-zero correlation. This weak correlation between observations far apart is often referred to as long memory. We provide ACF plots for over 150 lags for the returns series of three currencies in Fig. 1a-c. The plots of all the three currencies are consistent with the hypothesis of being generated by uncorrelated process. We repeat this analysis for absolute return and squared returns, a proxy of volatility, of three currencies and these are presented in Fig. 2a-c and 3a-c, respectively. Interestingly, the autocorrelations of the absolute residuals of the three currencies display extremely persistent autocorrelation however, squared returns of two currencies viz., IDR and TWD display persistent autocorrelation that is also suggestive of a form of long memory behavior.

Next, we examine long memory property in return and volatility series of three currencies using fractionally integrated models discussed above.

Long memory in returns: First, we estimated ARFIMA models for different orders (n, s) under the normal distribution to determine the adequate order of in detecting long memory property in returns series of the three currencies. All possible combinations for ARFIMA (n, ξ, s) with maximum n, s = 0, 1, 2 for each return series are considered for comparison.

| Table 2: | Unit root tests |

| |

| Number in parentheses represent the lag periods of the tests. * Indicate rejection at 5% significance level | |

| |

| Fig. 1(a-c): | Autocorrelation function of returns |

The conventional Akaike Information Criteria is used to choose the model that describes the data. Table 3 presents the best ARFIMA model chosen for the three currencies based on AIC. The preferred models for CNY, IDR and TWD are (1, ξ, 2), (2, ξ, 0) and (2, ξ, 2), respectively. The results indicate that the long memory parameter (ξ) is significantly different from zero for CNY and TWD. Hence, ARFIMA model supports long memory behavior in foreign exchange market of China and Taiwan. This suggests predictable behavior of exchange rate in these two countries and is inconsistent with the efficient market hypothesis.

The diagnostic statistics of Table 3 suggest large excess kurtosis and skewness. The large Jarque Bera statistics also suggest departure of standardized residuals from normality. If the conditional mean equations are correctly specified, then the Box-Pierce statistics should support the null hypothesis of the i.i.d. series.

| Table 3: | Estimation results of ARFIMA models for (a) CNY (b) IDR and (c) TWD |

| |

| Standard errors are in brackets corresponding parameter estimates. ln (L) is the value of the maximized Gaussian log likelihood and AIC is the Akaike information criteria. ARCH (5) represents the t-statistics of the ARCH test statistic with lag 5 based on residuals. * and ** indicate rejection at 5% and 10% significance level, respectively | |

| |

| Fig. 2(a-c): | Autocorrelation function of absolute returns |

Q (20) supports i.i.d. only in CNY. Further, the result suggests significant ARCH effect in the standardized residuals. This implies that modeling only level of return is not adequate for capturing the presence of long memory property in these currencies. Hence long memory property in volatility is also examined.

| |

| Fig. 3(a-c): | Autocorrelation function of square returns |

| Table 4a: | Estimation results of FIGARCH model for CNY |

| |

| Standard errors are in brackets corresponding parameter estimates. ln (L) is the value of the maximized Gaussian log likelihood and AIC is the Akaike information criteria. ARCH (5) represents the t-statistics of the ARCH test statistic with lag 5 based on residuals. P (60) is the Pearson goodness -of-fit statistic for 60 cells computed on standardized residuals. * and ** indicate rejection at 5 and 10% significance level, respectively | |

Long memory in volatility: Table 4a-c compare performance of the GARCH, IGARCH and FIGARCH specifications in modeling long memory property in volatility and determining the best fitting orders of (p, q).

| Table 4b: | Estimation results of FIGARCH model for IDR |

| |

| Standard errors are in brackets below corresponding parameter estimates. ln (L) is the value of the maximized Gaussian log likelihood and AIC is the Akaike information criteria. ARCH (5) represents the t-statistics of the ARCH test statistic with lag 5 based on residuals. P(60) is the Pearson goodness -of-fit statistic for 60 cells computed on standardized residuals. * and ** indicate rejection at 5 and 10% significance level, respectively | |

| Table 4c: | Estimation results of FIGARCH model for TWD |

| |

| Standard errors are in brackets corresponding parameter estimates. ln (L) is the value of the maximized Gaussian log likelihood and AIC is the Akaike information criteria. ARCH (5) represents the t-statistics of the ARCH test statistic with lag 5 based on residuals. P(60) is the Pearson goodness -of-fit statistic for 60 cells computed on standardized residuals. * and ** indicate rejection at 5 and 10% significance level, respectively | |

According to both AIC and SIC criteria, the FIGARCH model performs better than the two other models for all the three currencies taken in our study. The orders for best fitting FIGARCH model for CNY, IDR and TWD are (1, d, 0), (1, d, 0) and (1, d, 1), respectively. The estimation results of best fitting FIGARCH model of returns of three currencies are reported in Table 4a-c. As can be seen from the tables, for all the three currencies, sum of the estimates of β1 and Φ1 is very close to one, indicating that the volatility process is highly persistent. For the FIGARCH model, the estimate of long memory parameter (d) is found to be significantly different from zero and is within the theoretical value, indicating the volatility exhibits a long memory process in all the three Asian currencies.

| Table 5: | Estimation result of ARFIMA- FIGARCH |

| |

| Standard errors are in brackets below corresponding parameter estimates. ln (L) is the value of the maximized Gaussian log likelihood and AIC is the Akaike information criteria. ARCH (5) represents the t-statistics of the ARCH test statistic with lag 5 based on residuals. P (60) is the Pearson goodness -of-fit statistic for 60 cells computed on standardized residuals. * and ** indicate rejection at 5 and 10% significance level, respectively | |

Table 4a-c also present a set of diagnostic statistics which suggest that the standardized residuals exhibit skewness and excess kurtosis. Box-Pierce statistic tests, Q (20)and Qs (20), test whether standardized residuals and squared standardized residuals form the i.i.d. series. If the conditional variance equations are correctly specified, then the Box-Pierce statistics should support the null hypothesis of the i.i.d. series. Qs (20) statistic supports i.i.d. in all the three series. However, Q (20) supports i.i.d. only in CNY. Also, Pearson Goodness to fit test statistic P (60) is highly insignificant for all the three currencies for normal distribution. Thus the assumption of normal distribution is inappropriate to capture the dyanamics of exchange rate volatility of these three currencies. Hence the model is estimated with skewed student-t distribution in subsequent subsection. The FIGARCH model used appears to be inappropriate as the Box Pierce statistics Q (20), of the standardized residuals are correlated up to lag 20 for IDR and TWD, indicating mean equation is necessary for modeling long memory property. Hence, long memory is tested simultaneously in returns and volatility.

Dual long memory: In the preceding subsections long memory property in conditional mean and variance is investigated separately. However, long memory dynamics are commonly observed in both the conditional mean and variance. Therefore, we have analysed the dual long memory property in both the conditional mean and variance. In this regard, we have estimated the ARFIMA-FIGARCH model which gives a relationship between conditional mean and conditional variance of a process that simultaneously exhibit long memory properties. First the ARFIMA (n, ξ, s)-FIGARCH (p, d, q) model are estimated for all possible combinations of n, s = 0, 1, 2 and p, q = 0, 1. The results of best fit model have been presented in Table 5. The model has been selected on the basis of minimum AIC and SIC. Table 5 compares the estimates of ARFIMA-FIGARCH model under Gaussian and skewed Student’s t-distribution. The estimates of ARFIMA-FIGARCH model, long memory parameters, (ξ) and (d) are significantly different from zero for all the currencies. Also, LM ARCH statistic of Engle (1982) used to test the presence of the remaining ARCH effects in the residuals supports absence of ARCH effect in the all the three series. The skewed Student’s t-distribution is found to outperform the normal distribution for the above-mentioned three currencies, as the t-statistic of tail is highly significant. Further, lower value of Pearson’s goodness of fit statistics, P (60), of skewed Student’s t-distribution in comparison to Gaussian distribution reconfirms the relevance of skewed Student’s t-distribution for returns for CNY and IDR. However, P (60) does not support skewed Student-t distribution for TWD. Thus, the skewed Student-t distribution can be used to capture long memory property of conditional mean and conditional variance, simultaneously for CNY and IDR. The ARFIMA-FIGARCH model supports presence of dual long memory in CNY and IDR with skewed student-t distribution.

CONCLUSION

The study has examined the presence of long memory in daily nominal returns and volatility of three Asian exchange rates namely, Chinese Yuan (CNY), Indonesian Rupiah (IDR) and Taiwanese Dollar (TWD) in post reform period. For examining long memory in returns, first we estimated ARFIMA models. CNY and IDR have significant long memory parameter suggesting long memory in return series of above mentioned currencies. Next, GARCH, IGARCH and FIGARCH models were used to model volatility. The results suggest that the FIGARCH model fits the data better than the other two models. The result of the FIGARCH model indicates that the estimate of the long memory parameter is statistically significant, suggesting that the volatility is a long memory process for all the three currencies. To test the dual long memory i.e., long memory in returns and volatility simultaneously, ARFIMA-FIGARCH model is applied under both the normal and skewed student-t distribution. The estimation results indicate that the skewed student-t distribution outperforms the normal distribution for dual long memory model for CNY and IDR. Long memory parameters in both conditional mean and conditional variance are statistically significant for CNY and IDR, suggesting that the dual long memory property is prevalent in returns and volatility. However, TWD does not exhibit dual long memory. The results indicate inefficient foreign exchange market in China, Indonesia and Taiwan. Central banks of these countries intervene time to time in foreign exchange market to address unwarranted exchange rate movements stemming from temporary shocks. Though, such intervention protects the exchange rate from permanent changes but at the same time it leads to impaired price discovery.

REFERENCES

- Andersen, T.G. and T. Bollerslev, 1997. Heterogeneous information arrivals and return volatility dynamics: Uncovering the long-run in high frequency returns. J. Fin., 52: 975-1005.

Direct Link - Andersen, T.G. and T. Bollerslev, 1998. Deutsche mark-dollar volatility: Intraday activity patterns, macroeconomic announcements and longer run dependencies. J. Fin., 53: 219-265.

CrossRef - Baillie, R.T. and T. Bollerslev, 1989. The message in daily exchange rates: A conditional variance tale. J. Bus. Econ. Stat., 7: 297-305.

Direct Link - Baillie, R.T. and T. Bollerslev, 1994. Cointegration, fractal cointegration and exchange rate dynamics. J. Fin., 49: 737-745.

Direct Link - Baillie, R.T., T. Bollerslev and H.O. Mikkelson, 1996. Fractionally integrated generalized autoregressive conditional heteroskedasticity. J. Econ., 74: 3-30.

CrossRefDirect Link - Baillie, R.T., A.A. Cecen and Y.W. Han, 2000. High frequency Deutsche mark-US dollar return: FIGARCH representations and non linearities. Multinat. Fin. J., 4: 247-267.

Direct Link - Cheung, Y.W., 1993. Long memory in foreign-exchange rates. J. Bus. Econ. Stat., 11: 93-101.

Direct Link - Crato, N. and B.K. Ray, 2000. Memory in returns and volatilities of future's contracts. J. Futures Markets, 20: 525-543.

CrossRef - Fang, H., K.S. Lai and M. Lai, 1994. Fractal structure in currency futures price dynamics. J. Futures Markets, 14: 169-181.

CrossRef - Geweke, J. and S. Porter-Hudak, 1983. The estimation and application of long memory time series models. J. Time Ser. Anal., 4: 221-238.

CrossRef - Granger, C.W.J. and R. Joyeux, 1980. An Introduction to long memory time series models and fractional differencing. J. Time Seri. Anal., 1: 15-29.

CrossRef - Kihc, R., 2004. On the long memory properties of emerging capital markets: Evidence from Istambul exchange. Applied Financial Econ., 14: 915-922.

CrossRef - Morana, C. and A. Beltratti, 2004. Structural change and long range dependence in volatility of exchange rates, either, neither or both?. J. Empirical Fin., 11: 629-658.

Direct Link - Pan, M., Y.A. Liu and H Bastin, 1996. An Examination of the short-term and long-term behavior of foreign exchange rates. Financial Rev., 31: 603-622.

Direct Link - Tse, Y.K., 1998. The conditional heteroskedasticity of the yen-dollar exchange rate. J. Applied Econometrics, 13: 49-55.

Direct Link - Wang, C., 2004. Futures trading activity and predictable foreign exchange market movements. J. Bank. Fin., 28: 1023-1041.

Direct Link - Ling, S. and W.K. Li, 1997. On fractionally integrated autoregressive moving-average time series models with conditional heteroscedasticity. J. Am. Stat. Assoc., 92: 1184-1194.

Direct Link - Engle, R.F., 1982. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica, 50: 987-1007.

CrossRefDirect Link